The Bank's Preliminary Mortgage Approval - What to Focus On and What to Watch Out For

Once you've mapped out your financial needs, built an optimal mortgage mixture, gathered all the necessary documents, and run a winning negotiation, you start getting concrete offers from the banks. And those offers may well leave you confused. Why? Because the principle approval — the document spelling out the financing terms the bank is offering you — is packed with pages, financial jargon, data, and tables. If you're struggling to read the document you just received, and to know what to focus on and what to watch out for, don't worry — that's exactly what this article is here for.

A quick overview - principles of the new principle approval

The guiding principles behind the structure of the principle approval are uniformity of the offers and data across all banks, and identical, binding benchmarks for comparing the quality of a mortgage. We'll show how this plays out in a moment, but first, a bit of background:

📚Background: the evolution of the principle approval

The principle approval wasn't always such a long, intimidating document. At the end of 2021, the Bank of Israel decided to overhaul the mortgage market. The reform ended an era in which banks sold identical products under different names and used misleading, slanted calculations to push their wares.

The biggest advantage of the principle approval in its current form is that it standardizes the mortgage quality indicators: for each mortgage mixture, the bank presents the projected total interest rate, the estimated highest monthly payment, and the expected total payments. Estimated and uncertain as these figures are, they're your best tool for gauging the quality of your mortgage. They also let you judge how good your mortgage mixture, your mortgage broker, or your bank really is.

Standardized mortgage mixtures

In every principle approval, the bank presents three fixed, pre-defined mortgage mixtures. You have no control over their structure (you can only influence the loan duration [in years]). If you came to the bank meeting prepared and you know which mortgage mixture you want, the bank will also present a fourth mixture — the "proposed mix" — which is yours. We'll get into what each mixture can tell you in a moment.

The structure of the principle approval - what to focus on

Now let's take a closer look at how the principle approval is laid out and some simple ways to find your way around it.

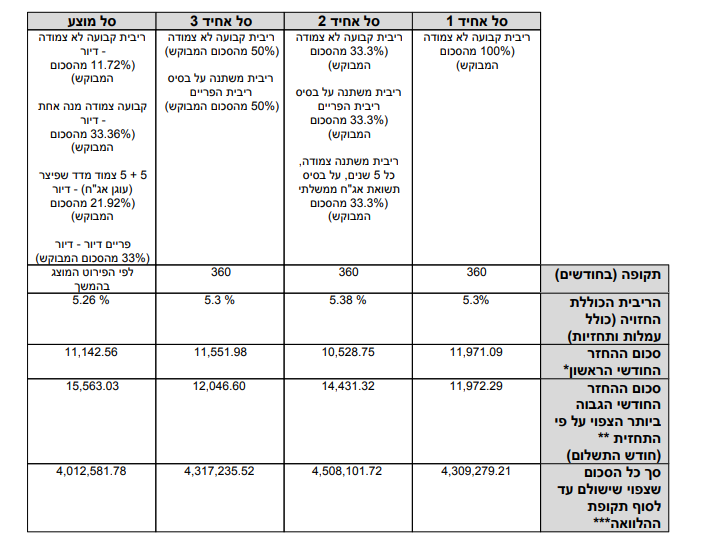

The first pages contain your personal details and the details of the property that serves as the bank's collateral. Right after that comes a table comparing the different mortgage mixtures — the three standardized baskets (standardized basket 1/2/3) and the proposed basket, which is your chosen mixture.

Pay attention to the figures in the table: the projected total interest rate, the highest monthly payment expected under the forecasts, and the total amount expected to be paid by the end of the loan. These are the parameters that describe the quality of the mortgage mixture.

This annual cost factors in macroeconomic changes: changes in inflation, in the Bank of Israel interest rate, in the yield on Israeli Government bonds, and so on.

Why are the words "projected" and "expected" used?

What does "projected" actually mean? Does the bank not know how much we'll pay? Is there room here for the bank to game things? Not at all.

Remember that, except for one loan — the fixed unlinked (KALATZ) track — every other loan in the mortgage depends on parameters you have no control over whatsoever. For example:

- The interest rate on the prime-linked loan depends on the Bank of Israel interest rate, which is updated eight times a year.

- The principal on the fixed CPI-linked (KATZ) loan moves with inflation, which is updated every month.

- The interest rate on the variable rate unlinked CPI (MALATZ) every five years loan depends on the yield on government bonds over a five-year period, and is updated every five years.

If you knew nothing about any of this, you might assume that the prime rate never changes and inflation stays at zero over the life of the mortgage, in which case the monthly payment would effectively stay flat. But that's wrong, and more importantly it's dangerous — because anyone who assumes it could wake up to find the monthly payment climbing out of control.

Fortunately, the Bank of Israel has stepped in and requires all banks to work with the same set of economic assumptions and forecasts — which estimate how the economic variables (prime rate, inflation, and so on) will move over the next thirty years. Those forecasts, in turn, drive the changes in the payment and cost of your mortgage. The file of changes and economic assumptions is updated every 15 days on the Bank of Israel website.

OK. So what is "the total amount expected to be paid until the end of the loan term"?

Based on the Bank of Israel's assumptions and forecasts, the bank calculates how much your mortgage will cost you, including expected interest rate changes and indexation — assuming you stay with it to the end and don't refinance or make early prepayments along the way.

What is the "projected total interest rate" in the principle approval?

The projected total interest rate is the internal rate of return (IRR - Internal rate of return). What does that actually mean? Unfortunately there's no way to explain it well enough in a single paragraph, so we'll point you to the explanation of IRR on Khan Academy. What we will say is that it involves discounting the estimated total payments (including CPI indexation and interest rate changes). Either way, here's what matters: the lower this number, the cheaper your mortgage.

What is the "highest expected monthly payment" and why does it differ from the "first monthly payment"?

As we said above, except for the fixed unlinked (KALATZ) loan, the payments on your other loans depend on external economic variables. If the Bank of Israel interest rate rises, the payment on your prime-linked loan rises. If inflation rises, the payments on your CPI-linked loans rise.

You'll notice that the number shown here is usually larger than the first monthly payment. It's important to understand that with a mortgage, how the monthly payment evolves over the years matters more than the payment you agree on with the bank at the very start.

You have to prepare for your payment rising along the way, and this figure helps you see how much it's expected to rise (if at all). On top of that, how you build the mortgage mixture affects how high the maximum payment ends up.

When can the comparison table not be used?

The comparison table is a fantastic tool for figuring out whether your mortgage mixture is good, which bank is the most attractive, how much you'll pay down the line, and more. But there are cases where you can't use it, or where the data isn't accurate or up to date. Let's go through when the comparison table can't be used.

If you're going to make a move on the mortgage (an early prepayment, a refinance down the road), the parameters we described above are beside the point. The bank doesn't know about these plans, and even if it did, there'd be nothing it could do or change. The analyses the bank presents assume you'll stay with the mortgage to the very end and never make prepayments or larger payments. If that's not the case, just ignore the figures in the comparison table and find another way to compare the offers. (Did you know we analyze your mortgage mixtures for you, taking all these changes into account?)

If you got an offer from bank A between the 1st and 15th of the month, and then an offer from bank B between the 16th and the 31st, you can't compare the two. Every half-month, the Bank of Israel updates the economic variables afresh.

To assess the quality of a mortgage mixture, the banks have to use the economic models available to them at that moment. If mixture A is assessed on the expectations from the first half of the month and mixture B on the expectations from the second half, you can't compare the offers, because each one rests on a different set of variables and macroeconomic observations. You need to ask bank A to reissue an updated version of the mixture, or run both mixtures through a mortgage calculator that evaluates them under the same macroeconomic assumptions.

Some banks offer loans in foreign currency — for example, loans whose interest rate is linked to the euro or the dollar. These loans react to changes in the exchange rate of the dollar or euro against the NIS. The daily, volatile trading in these currencies makes it impossible to forecast future changes in the payment at all, so the banks treat them as a fixed unlinked loan — that is, a loan whose monthly payment never changes. That's obviously wrong; no loan is more volatile than these — but for the cost calculation the bank treats them as fixed unlinked. It's a genuine distortion that makes such a loan look safer than it is. So if you have foreign-currency-linked loans in your mixture (and you'd better have a very good reason for it), ignore what the comparison table shows you.

What are the standardized mortgage baskets published in every preliminary approval we receive?

Let's go through the three standardized baskets and weigh the pros and cons of each. If you'd rather, you can skip straight to our critique of them and how well they actually fit your mortgage.

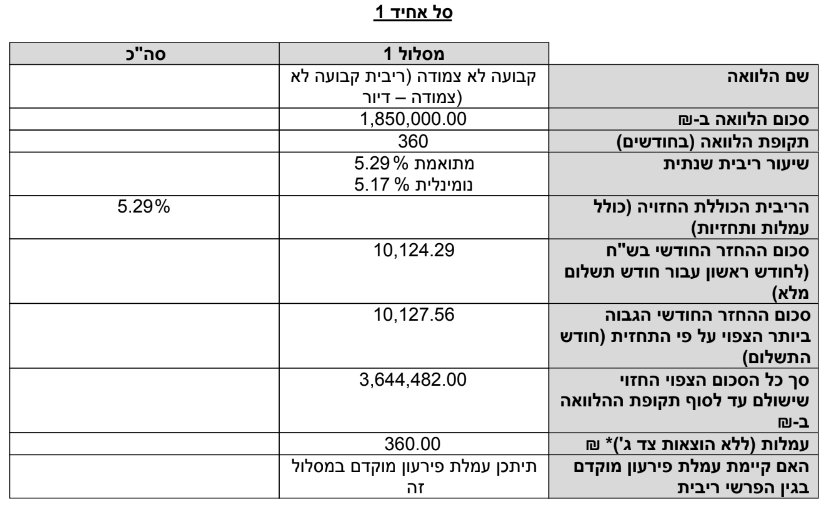

Standardized basket 1 - 100% fixed unlinked loan - conservative and extreme

The first mortgage mixture offered to us (standardized basket 1) consists of a single loan. The entire amount sits at a fixed unlinked (KALATZ) interest rate. This mixture gives you 100% certainty about the expected payments and the total interest you'll pay over the life of the mortgage. The monthly payment is fixed and never changes, under any circumstances.

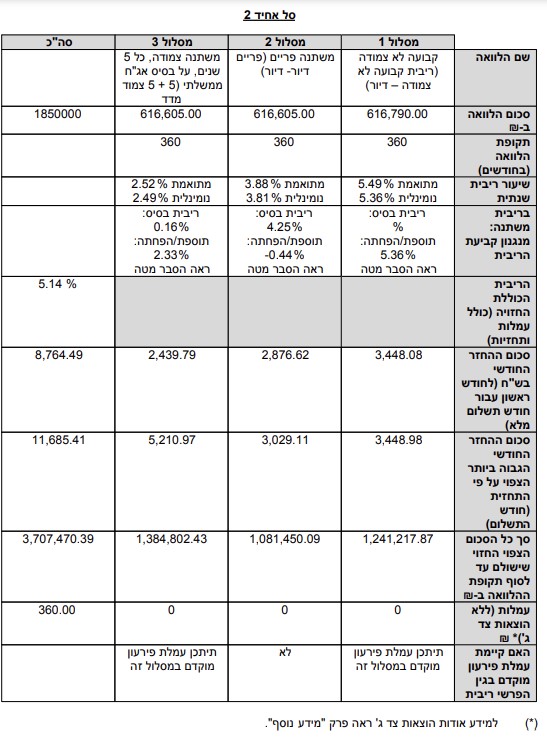

Standardized basket 2 - one third fixed / variable / prime - a watered-down version of the banks' thirds mix

The second mortgage mixture is a watered-down version of the popular thirds mix that banks used to sell — until 02/22 (when the war in Ukraine broke out). The loan amount is split equally across three tracks: fixed unlinked (KALATZ), prime-linked and variable CPI-linked (MATZ).

Why watered-down? Because in the banks' original thirds mix, they at least shortened the fixed unlinked loan to improve the interest rates. Here, in the name of uniformity, all the loans share the same duration. We'll get into the downsides of that shortly.

The risk level this mixture aims for is moderate, since there's a degree of risk diversification between the tracks deemed risky and those deemed relatively safe.

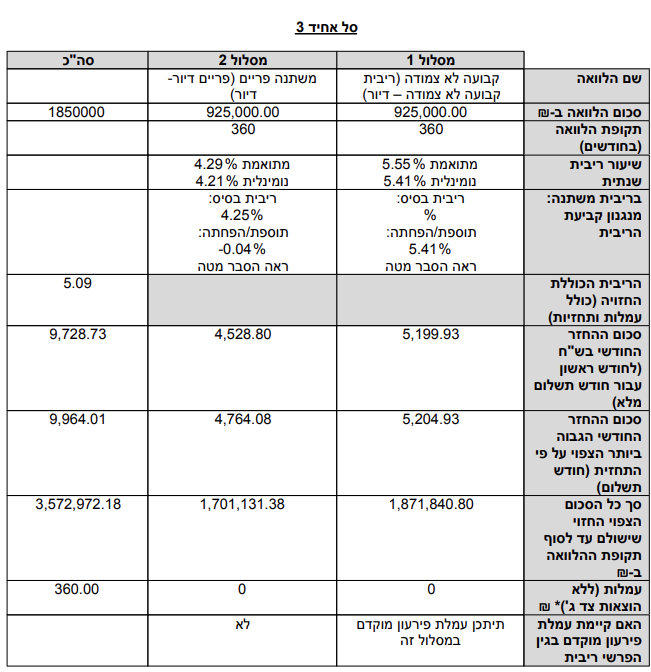

Standardized basket 3 - half prime-linked and half fixed unlinked

In the third basket the loan amount is split equally between the prime-linked track and the fixed unlinked (KALATZ) track. In effect, it splits evenly between the most volatile track (prime-linked) and the least volatile one.

Which of the standardized mortgage mixtures is most suitable for me? Which one should I choose?

The upside of showing these three basket mixtures is that they offer a tiny glimpse of just how rich mortgage planning can be. It's interesting to see how a different combination of tracks — all for the same loan duration — produces different initial/maximum monthly payments and completely different costs.

Unfortunately, that's the only good thing we have to say about this part of the reform. Let's start with the disadvantages.

First, there's no situation in which you can fairly compare the tracks. How is it fair to compare one track with another when the monthly payment isn't even the same?

Look at the table above. There's an 18% difference between the cheapest track (mixture number 4, which also runs for 360 months) and the most expensive mixture. As we explained in the article on the optimal mortgage mixture, you can only compare the quality of mixtures if all the conditions are equal — the same monthly payment and the same market spread. Here we're being asked to compare apples to oranges.

If we take basket mixture 2 and bump the monthly payment up to match basket mixture 1, we can produce a loan that's much cheaper and shorter (and, by the way, also riskier).

We don't think you can look at this table and say which mixture suits you better or worse.

In our view, boiling mortgage planning down to a handful of mixtures to "help" borrowers actually hurts them. Who said these are the best mixtures? Does someone planning a mortgage for an "exit" (meaning they'll sell the property soon) need the same mortgage as someone stretched thin who needs a safer one?

Having these mixtures in every principle approval creates a psychological "anchoring bias" — they become the reference point against which you judge every other mixture. But are they good enough to serve as that anchor? No. Not at all.

Unlike the basket mixtures, there's a very good reason the vast majority of mortgage mixtures (the kind you'll see on our mortgage forum) are made up of loans of different durations. It's not because the banks or mortgage brokers want to complicate things and confuse you. Each loan differs from the next in several respects:

- The price of the loan — the monthly payment it takes to carry that loan.

- The interest rate on the loan.

- The risk of the loan — how likely the payment is to rise above the initial payment, and by how much.

- How profitable the loan is for the bank (that is, its market spread).

- The early prepayment cost of the loan.

And so on...

So when we set the loan durations (along with the amount allocated to each), we control how much each loan influences the quality of the overall mixture. Beyond the allocated amount, shortening a loan's duration increases its weight and its impact on how the mixture performs. Lengthening it does the opposite.

Locking every loan to the same duration seriously undermines your ability to plan an optimal mortgage mixture.

Not that we think the answer is to present 10 different basket mixtures, but when you only show three set mixtures, there are other useful mortgage tracks that never get a look-in and stay out of sight. Here's a far-from-complete example:

- A variable rate unlinked CPI (MALATZ) loan, suited to those planning to refinance the mortgage later, who want to minimize the early prepayment fee but worry about inflation. Or:

- A government-subsidized mortgage (ZAKAOT) loan, which grants a discount on the early prepayment fee to anyone who includes it in the mixture. Or:

- A variable-rate loan linked to the euro, suited to those who earn their income in foreign currency. Or:

- A variable-rate loan that resets every two and a half years — for those who want to make an immediate early prepayment (teaser-rate loan).

How can you use the principle approval to understand how good your offer / your broker / your bank is?

On the flip side, the principle approval is a huge help to anyone who knows which mortgage mixture they want and what they're trying to achieve. In fact, thanks to its comparison table, you can tell whether your mortgage mixture, your mortgage broker, or your bank is good or not. How? Read on.

How can you use the principle approval to find out which bank gave you the best interest rates?

As you'll recall, all banks have to analyze the mixtures using the same set of macroeconomic assumptions. So when you receive offers from several different banks, and assuming the mixture is identical across all of them except for the nominal interest rate on each track, you can tell which bank gave the best offer — based on the projected total interest rate. The cheapest bank is the one with the lowest projected total interest rate.

Remember, you can only make this comparison for approvals issued during the same half of the month.

How can you use the principle approval to find out whether the mixture you received is a good one?

To justify building a mortgage mixture that differs from the existing basket mixtures, the mixture you build has to add value beyond the standardized mixtures you received.

If, for example, the goal of the mixture built for you is to minimize the repayment ratio, then using the comparison table, check that at least one of the following conditions holds:

- The proposed mix must be cheaper, in the total amount expected to be paid until the end of the loan term, than all three other mixtures.

- The projected total interest rate of the proposed mix must be lower than the projected total interest rate of each of the other standardized basket mixtures.

- If condition (a) or (b) isn't met — meaning there's a basket mixture cheaper than the one we built, on either the projected total interest rate or the total amount expected to be paid until the end of the loan term — then our proposed mix must at least have a lower monthly payment than that basket mixture.

An excellent mortgage mixture is one that meets both conditions (a) and (b) and on top of that has a lower monthly payment than all the other mixtures.

Note: for a fair comparison, make sure the duration [in years] of the basket mixtures is roughly the same as the duration of the mixture you built.

How can you use the principle approval to find out whether a mortgage broker can help you?

Thinking about hiring a mortgage broker and want to know whether they can build a better mortgage mixture than yours? Now you have a real way to assess that. All banks are required to provide mortgage calculators based on the Bank of Israel's economic assumptions. Ask the broker to show you, using the banks' independent calculators, how the mixture they're proposing beats the one you currently have in hand. If they've built a mixture that meets the conditions above (and assuming the same interest rates are available), then their mixture is better than yours, and their services are worth it.

Want a broker who'll give you the best mortgage mixture? That's us. Learn about our services now.

Good luck!