Early Prepayment Fee - What It Is and How to Minimize It

One of the most common questions in mortgage planning and management is how and when to pay it off ahead of schedule. Since most of us think of a mortgage as a bad thing (not necessarily fairly), it's only natural to look for proactive ways to shrink it — beyond the regular monthly payments. Using available capital to reduce the outstanding mortgage balance, outside the monthly payments and after you've already taken out the mortgage, is called early prepayment (of a mortgage).

The catch is that making an early prepayment means paying fees to the bank — and the largest and most talked-about of these is the early prepayment fee.

This article covers what the early prepayment fee is, how it's calculated, and — more importantly — how to minimize it, whether by planning a mortgage mixture built for prepayments from the start, or through steps you take after the mortgage is already in place.

First, what is the early prepayment fee?

Banking Ordinance (Early Repayment of Housing Loans) - 2002

When you take out a mortgage, you enter into a contract with the bank. The contract spells out the financing terms you'll get — the amount, the loan duration, and so on. When you ask to pay down your debt ahead of schedule, you're departing from the terms you signed, so the bank asks to be compensated — in the form of an early prepayment fee.

The early prepayment fee represents the economic loss the bank takes once you repay the loan. That loss (and the fee) can reach tens of thousands of NIS, which is exactly why we want to learn how to keep it down.

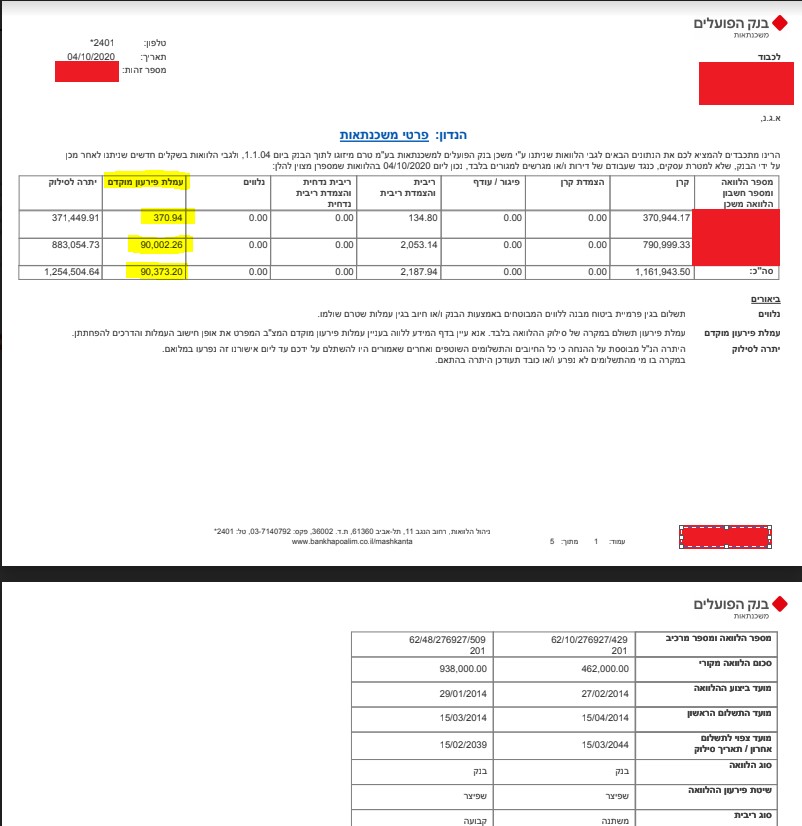

The attached screenshot — easily the most extreme example we've ever come across — shows an early prepayment fee of 90,000 NIS! Think about it: if your monthly payment is 5,000 NIS, that's 18 months of payments down the drain. Brutal!

📚What factors affect the discounting fee — a technical section, optional reading!

The way the early prepayment fee is calculated is described in the Banking Ordinance of 2002. It's a fiendishly complex calculation — which is why there are so few calculators and professional resources on the subject. You're welcome to read the text of the law if you like; we think it's heavy going, so we'll lay out the factors that affect the fee and its size here — but feel free to skip to the next section, because this is where the headaches begin.

Explanation of the early prepayment fee formula

The early prepayment fee is the difference between the discounted present value of the payments at the current interest rate (the rate on the prepayment date) and the discounted present value of the payments at the interest rate on the day the mortgage was taken out or at the average mortgage interest rate on the day the mortgage was taken out — whichever is lower. The formula for calculating the early prepayment fee is shown here (for the case where the lower rate is the mortgage rate on the day it was taken out). Let's walk through what we're looking at:

The early prepayment fee is calculated as the discounted sum of the payments (B_i) at the monthly interest rate (A) on the prepayment date, plus the discounted amount remaining to be repaid at the rate change date (if there is one), minus the discounted sum of the payments (B_i) at the lower of: the interest rate on the day the mortgage was taken out, or the average mortgage interest rate on the day the mortgage was taken out, plus the discounted amount remaining to be repaid at the rate change date (if there is one).

Later in the article we'll explain how to calculate the monthly interest rate A and the average rates R.

What is discounting of payments?

First, what is discounting of payments? Discounting is how the value of money shrinks over time. To see this, take the following example: you lent a friend 1,000 NIS two weeks ago, and now it's time for them to pay you back.

Which would you rather have? The full debt (1,000 NIS) now (option A)? Or 500 NIS now and 500 NIS a year from today (option B)?

Almost all of us would rather have the money now (option A) — so we can put it toward whatever we need. Preferring option A over option B shows that when we get the money matters to us. In other words, the value of money depends on time.

Which would you rather have? The full amount (1,000 NIS) now (option A)? 500 NIS now and 520 NIS a year from today (option B)? Or 500 NIS now and 560 NIS two years from today (option C)?

Now it's a trickier question. How do we know which is the best deal? Discounting is the way to answer it. When we "discount" a series of payments, we bring all the payments to a single point in time.

Payment Discounting Calculator

Compare payment options by their present value

For example, in option C above, we calculate (discount) the value of the second payment (560 NIS), due in two years, as if it were received today. We divide the amount we'll receive by the discounting rate raised to the power of the number of periods.

Example: if the discounting rate is 5% per year and the number of periods is two (because two years have passed), we divide 560 by 1.05 raised to the power of two.

The general formula for discounting (finding the present value of a series of payments

Option B: receiving 500 NIS now and 520 NIS in one year:

Option C: receiving 500 NIS now and 560 NIS in two years:

In other words, at a 5% discounting rate, option B actually loses us money. Meanwhile, getting 1,007.9 NIS today versus 500 NIS today and 560 NIS in two years — these are exactly the same thing.

The factors that affect the early prepayment fee — worth reading!

Let's boil the technical section down to the factors that drive the early prepayment fee. Don't skip this part — it's the foundation for planning a mortgage mixture that minimizes the early prepayment fee.

- The number of years remaining until full loan repayment — the longer the loan duration (N), the higher the discounting fee.

- The average interest rate on the prepayment date (A) — the lower the rate on the day you prepay the mortgage, the higher the fee.

- The average interest rate on the day the mortgage was taken out (R) — the lower the rate, the lower the prepayment fee.

The fee level across the different mortgage loan tracks

Not all mortgage loans are created equal. Some are exposed to a smaller fee than others, and vice versa. Let's run through the different loans:

- Prime-linked / Euro / Makam loans — prepaying these loans carries no early prepayment fee, because the rate changes more often than once a year (section 4.2 of the Banking Ordinance of 2002).

- Government-subsidized mortgage (ZAKAOT) — prepaying these loans carries no early prepayment fee (section 2 of the Banking Ordinance of 2002), and on top of that, having this loan in the mortgage mixture reduces the early prepayment fee on other loans (section 8 of the Banking Ordinance of 2002).

- Variable-rate loans — prepaying these loans carries a reduced early prepayment fee, because the payments are summed only up to the rate change date (section 4.1 of the Banking Ordinance of 2002).

- Fixed-rate loans — prepaying these loans means paying the full early prepayment fee.

How to minimize the early prepayment fee

As noted, the early prepayment fee can soar to tens of thousands of NIS, so we'll want to act to keep it down. There are things worth doing and knowing right when you build the mortgage mixture — but if you didn't, there are still a handful of steps you can take to reduce the fee after the mortgage is in place.

Minimising the fee before taking out the mortgage

The most effective way to reduce the early prepayment fee is to build a mortgage mixture that minimizes it from the start. We'll now go through a number of methods and techniques that let you pay less. The first method minimizes prepayment fees when you already know you'll be prepaying money in the future. The rest are meant to let you minimize the prepayment fee if you choose to prepay later on.

Method 1 — when planning a future prepayment, include a variable-rate loan in the mortgage mixture

If you know, even before taking out the mortgage, that you're going to make a future prepayment (say, an upcoming work bonus, help from family, proceeds from selling a property, and so on) and you can estimate how much you'll prepay, then include variable-rate loans or a prime-linked loan in the mortgage mixture up to that amount. A prime-linked loan guarantees you won't pay a fee at all, but a variable-rate loan boosts the bank's profitability (the market spread) and lets you land better interest rates on the other tracks — the ones you'll be living with for many more years.

Method 2 — include a government-subsidized mortgage (ZAKAOT) in the mortgage mixture

As noted, including a government-subsidized mortgage (ZAKAOT) in the mortgage mixture reduces the early prepayment fee when you repay other loans in the mixture. So if you're eligible for this loan, consider including it. Just keep in mind that the government-subsidized mortgage has other drawbacks when it's part of the mixture.

Method 3 — shorten fixed-rate loans

As described above, the loan term affects the fee charged. The fee on a short loan will be lower than on a long one. So when planning a mortgage mixture designed to reduce the early prepayment fee, shorten the fixed-rate loans as much as you can. There's no point shortening the non-fixed-rate loans, because some of them carry no fee at all, and shortening their term raises their monthly payment, which forces you to extend the fixed-rate loans — driving their fee up.

A note in passing: shortening the term of fixed-rate loans is the right move when it comes to minimizing early prepayment fees, but it's not necessarily the right move when it comes to building an optimal mortgage mixture.

Method 4 — use CPI-linked loans

As noted, the lower the interest rate (or the average interest rate) on the day the mortgage was taken out, the lower the early prepayment fee. In other words, if you can bring the interest rate down, you'll pay a lower fee. One way to do that is to switch to loans linked to the Consumer Price Index (CPI) — that is, a fixed CPI-linked loan (KATZ).

Method 5 — balance interest rates during negotiation

At the end of the interest-rate negotiation, once you know which bank will give you the mortgage, you can ask the mortgage banker to tweak the interest rates and minimize the chance of paying an early prepayment fee. Ask them to raise the rate on the prime-linked loan — which carries no early prepayment fee — and lower the rates on the fixed-rate loans.

Minimising the fee after taking out the mortgage

OK — you've already taken out a mortgage and you want to pay it down? Let's look at how to minimize the fee as much as possible now that the mortgage is in place. To do that, we need to dig even deeper into how the average interest rate on the prepayment date is calculated. We'll see that the timing of your prepayment is critical to the size of the fee.

How average interest rates for prepayment are calculated — important to read and understand

To understand how to calculate the average interest rate on the prepayment date, let's work through an example. Pay close attention to the figures — they matter!

Let's say the date we want to prepay is 30/9/2021. Suppose we took out a fixed unlinked (KALATZ) loan at 3.55% on 08/06/2020 (that being the date the money moved from the bank to the seller). The last payment falls on 15/6/2034 — 14 years after the loan began. We want to figure out the discounting rate on the prepayment date.

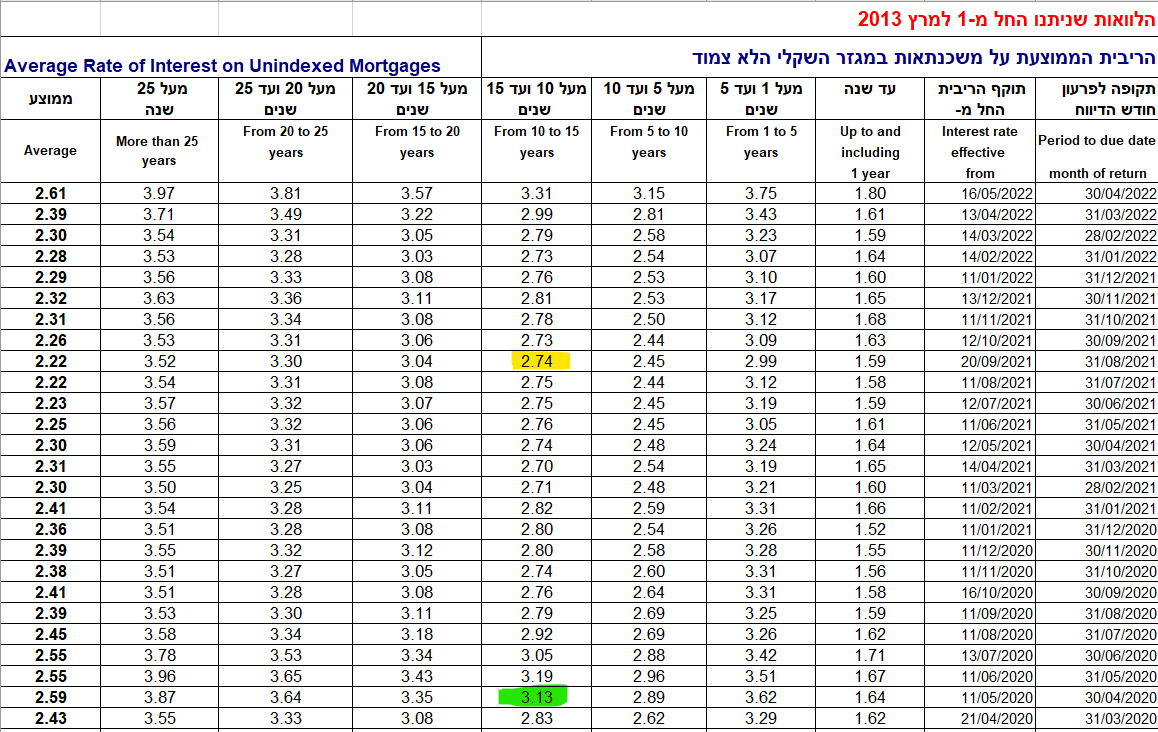

We head to the Bank of Israel website, where average mortgage interest rates are published each month (CPI-linked and non-CPI-linked). Since we want to prepay a loan that's not linked to the Consumer Price Index, we look at the unlinked shekel sector.

Since the remaining term of the fixed unlinked (KALATZ) loan is 14 years, it falls in the 10-to-15-year category. The average interest rate on such a loan when it was taken out (8.6.2020) was 3.13% (highlighted in green). A year and two months later, the time left to repay the loan has dropped from 14 years to 12 years and ten months — still within the 10-to-15-year interest-rate band — so the average interest rate on the prepayment date (30.9.2021) is 2.74%.

Since the average interest rate when the mortgage was taken out (3.13%) is lower than the rate on the loan we actually took (3.55%), we use the average rate from the day the mortgage was taken out.

In other words, the discounting rates on the prepayment date are 2.74%, and the discounting rates on the origination date are 3.13%.

If you followed all that, you're ready to bring your early prepayment fee down!

Methods for reducing the early prepayment fee after taking out the mortgage

All the methods described here come down to holding off on your prepayment until a certain point in time. Waiting can change the discounting rate or earn you a discount. The downside is that interest rates in the economy can shift completely — wiping out any benefit from waiting.

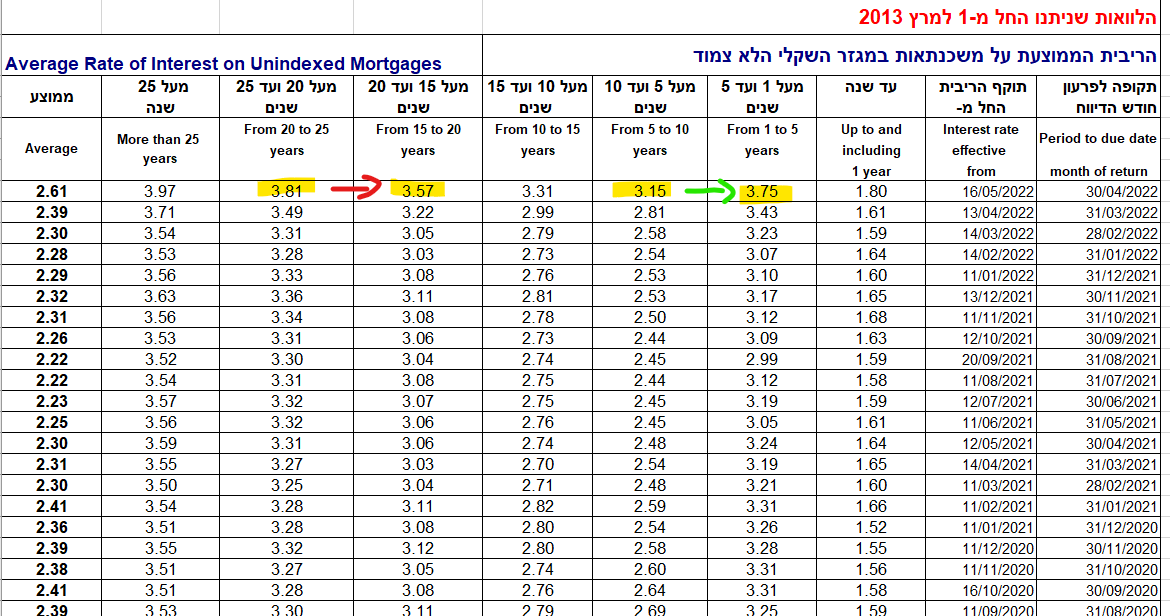

Method 1 — prepay fixed-rate loans just before or after crossing a five-year maturity bracket boundary

If you look at the table above, you'll see that when we cross a maturity bracket (for example, moving from the 20–25 year bracket to the 15–20 year bracket — highlighted with the red arrow — or from the 5–10 year bracket to the 1–5 year bracket — highlighted with the green arrow), the average interest rate changes (it usually falls).

If the average interest rate falls (the red transition), the gap between the discounting rate (highlighted in yellow) and the rate on the mortgage origination date widens — and a wider gap means a bigger prepayment fee. On the other hand, if the average interest rate rises (the green transition), the early prepayment fee shrinks!

Method 2 — wait for a fee reduction at the end of a tenure period

Section 8 of the Banking Ordinance of 2002 covers reductions in the early prepayment fee that you're entitled to once your loan has built up enough tenure.

The reduction depends on two things: whether there's a government-subsidized mortgage (ZAKAOT) in the mixture, and how much time has passed so far. We've included a discount calculator to help you see whether you qualify for a discount and how big it is.

Are you close to completing a minimum period that would earn you a discount, or bump it up? If so, it's worth waiting.

Method 3 — be careful when prepaying non-CPI-linked loans where the time remaining until the rate update / end of the loan is less than one year

The breakdown of interest rates for non-CPI-linked loans has one small but important addition compared to the breakdown for CPI-linked loans: a separate column showing the interest rate on loans whose remaining term is up to one year.

This column was meant to capture the average interest rate of the prime-linked loan, but in practice it created a very dangerous distortion that can send your prepayment fee shooting up.

Imagine you have a five-year variable-rate unlinked loan. Four years have already passed, and the rate resets in one year — so the time left until the rate update is less than one year. Under the Banking Ordinance, we have to compare the rate on this loan against the average rate on loans whose remaining term is less than one year.

The problem is that this average rate can be completely different — because it reflects the rate of the prime-linked loan, not variable-rate unlinked loans — so the discounting rate surges. Make sure you prepay before you hit this danger zone.

Want to plan a mortgage mixture that makes life easier if you decide to prepay down the road? Head to our mortgage calculator and design a mixture that minimizes your exposure to prepayment fees.

Good luck!