The Optimal Mortgage Mix

We need money from the bank to buy our home. When we get to the bank, the mortgage banker will ask what form we'd like to receive the money in. In practical terms, the banker is asking what our mortgage mixture is.

We'll explain how to choose it in a moment. There are over one hundred billion ways to build a mortgage mixture (really!). In that endless sea of options, how do we know which mortgage mixture is right for us? And what makes a mortgage mix optimal in the first place?

Wait — what exactly is a mortgage mixture?

When it's time to choose our mortgage, we can put together several loans on different terms. That combination of loans is what we call a mortgage mixture.

The number of loans can range from just one to about a dozen (in case you've really lost it). In practice, the limit on how many loans make up the mixture is (almost) never technical — it comes down to how willing the mortgage banker is to go along with your requests.

How do these loans differ from one another? In their payment terms, their stated interest rates, the type of indexation, and more. We'll get into that in depth later. The way we combine the loans shapes how the mortgage behaves. Most obviously, the mixture sets our initial monthly repayment — but just as important, it also drives the mixture's risk level, its volatility, and its total cost.

The upside: Building a well-crafted mortgage mixture brings down the cost of the mortgage itself, because you can combine loans in a way that plays to the strengths of each track. On top of that, combining several loans lets you tailor the mortgage to your needs much more precisely.

The downside: Building a mortgage mixture gets complex and confusing. It's hard to figure out how to match the mixture and the loan types to your needs.

We're in the business of busting myths and rules of thumb, so the myth we want to bust here is that some loans are simply better than others. That's not true. Every loan track has its pros and cons. So when we build a personalized mortgage mixture, we have to combine the loans the right way to minimize each track's downsides and maximize its upsides.

How do we know we have a quality mortgage mixture?

To choose the right mixture out of all the others, we need a way to measure them that tells us whether mixture A is better than mixture B.

When we analyze your mortgage offer and publish it on the mortgage forum, one of the things we use to compare mixtures is the repayment ratio.

Given two mixtures to compare, let's look at the total interest payments in each:

| Mixture A | Mixture B | |

|---|---|---|

| Total interest payments | 300,000 NIS | 500,000 NIS |

Table 1: Total cost of interest

So the first mixture is the better, more sensible choice.

Sounds a bit too simplistic, doesn't it?

You're right — that's not a thorough enough answer. Let's explain why by taking another look at those same two mixtures:

| Mixture A | Mixture B | |

|---|---|---|

| Initial monthly repayment | 5,500 NIS/month | 4,500 NIS/month |

Table 2: Initial payment constraint

Now it's clear why the first mixture is more expensive: its monthly payment is lower, so the principal (the loan balance) shrinks more slowly, which means the interest payments are larger.

If we took the first mixture and added the same 1,000 NIS that's paid in the second one, might it actually come out ahead? It just might.

Here's another example. Suppose the two mixtures are completely identical, and we received interest rate offers from two banks. One bank is much further along in the negotiation — this is already its third offer, the rates are very good, and the initial monthly repayment is lower than the second bank's, where we've only received one offer so far.

| Bank A | Bank B | |

|---|---|---|

| Offer received | Third offer | First offer |

Table 3: Negotiations constraint

Does that mean the first bank is better? Not necessarily. Comparing the two banks is only valid if they're both at the same stage of negotiation.

How do you define an optimal mortgage mix?

So how do we compare mixtures properly and arrive at the optimal mortgage mix? Here's our take:

The optimal mortgage mix is the one that drives the total cost (*) lower than any other mixture with the same constraints.

The total cost can be measured in several ways: total interest and indexation payments, the repayment ratio, or the internal rate of return (IRR) of the mortgage.

An example from the world of cars

Let's borrow an example from a different field. Say we want to buy a new car, and we're torn between a Mercedes and a Toyota Corolla. It's hard to know which to pick. Maybe we'll base our choice on the price of the car? In that case, the Toyota Corolla wins by a landslide.

Hold on... the odds of us actually making that comparison are basically zero. You simply can't compare these two cars. Sure, both are motorized, both burn fuel, and both have a monthly operating cost. But they're worlds apart. They don't target the same buyers, they don't come with the same feature package, and they don't deliver the same performance.

So maybe we should compare the Mercedes to an Audi? Or a BMW? We can agree those are far more sensible comparisons. In other words, for a price-based comparison to make sense, we compare only cars in the same luxury category. That's the constraint. And that's exactly how to approach the search for the right mortgage mixture among all the available options.

How do you build an optimal mortgage mix?

When we build a mortgage mixture during the mortgage advisory process, we run mathematical algorithms that search for the best mixture within a defined set of financial limits and constraints. In other words, we look for the mixture with the lowest total interest payments among all the possible mixtures that meet the following constraints (and this is only a partial list):

- Fixed initial monthly repayment — for example, we look at all mixtures with an initial monthly repayment of 5,000 NIS.

- Fixed maximum monthly repayment — for example, we look at all mixtures whose maximum monthly repayment never crosses 7,000 NIS a month over the years.

- The same market spread

- Special conditions — all mixtures with a grace period of 3,000 NIS for 30 months, and/or redemption of a study fund after 60 months, and/or a teaser-rate loan, and/or a balloon loan, or anything else we can dream up...

These are only some of the constraints; there are more, and they come out during the needs assessment process. To sum up what we're doing here: we define a set of constraints on the mortgage — initial monthly repayment, maximum monthly repayment, payment terms, loan duration, exposure to variable-rate tracks, exposure to the prime-linked track, use of non-bank loans, use of government-subsidized mortgage (Zakaot) funds, and so on — and out of all the mixtures that meet those constraints, we pick the one with the lowest total interest payments.

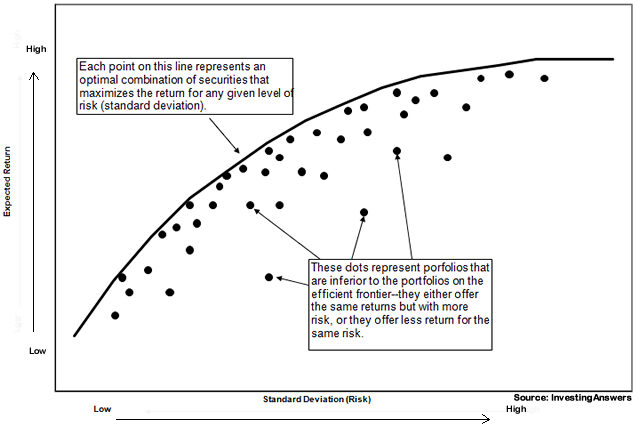

The Efficient Frontier is a concept from Modern Portfolio Theory developed by Harry Markowitz. It describes the set of optimal investment portfolios — the ones that offer the highest possible return for a given level of risk, or, equivalently, the lowest risk for a given level of return. Any portfolio on the Efficient Frontier is considered efficient, while one below it is sub-optimal — because there's another portfolio with the same risk but a higher return.

Application to mortgages: In much the same way, you can build an "Efficient Frontier" for mortgages, where the axes are total cost (interest) versus risk (exposure to swings in the monthly payment or to interest rate changes). An optimal mortgage mix is one that minimizes the total cost for the level of risk the borrower is willing to take — for example, a combination of a fixed-rate track (low risk, higher cost) and a variable-rate track (higher risk, lower expected cost).

About Harry Markowitz: Harry Markowitz (1927-2023) was a Jewish-American economist who won the 1990 Nobel Prize in Economics for developing Modern Portfolio Theory. First published in 1952, his work remains the theoretical foundation of investment portfolio management to this day.

Our critique of the optimal mortgage mix concept

Is the mortgage mixture really the thing that needs to be optimized? Maybe it's our lifestyle? And maybe what we should really be improving is our cash flow?

After thousands of conversations with clients, our sense is that chasing the cheapest mortgage can lead people to skip the first and most important stage — financial planning.

It's true that the higher your monthly payment, the better your mortgage: it'll be cheaper and shorter. But does that mean you should keep ratcheting up the cash-flow risk again and again? We don't think so. Is it worth landing a cheap mortgage if you pay for it with a stressful, hand-to-mouth life — every spare shekel going to the monthly payment and nothing left to live on? We don't think so.

What you have to do is very precise financial planning that fits your financial goals. For example, deciding what monthly payment you want, and how much down payment to put on the property before taking out a mortgage.

Good luck!