This article walks through the ins and outs of mortgage refinancing. What is mortgage refinancing? What's the difference between internal and external refinancing? When is it worth refinancing? What's the actual procedure? And is refinancing a mortgage like taking out a new loan?

Step one: Working out whether you need to refinance - what is mortgage refinancing?

In mortgage refinancing, we "reopen" the terms of the deal (the loan terms, which are the mortgage terms) with the bank that granted us the mortgage, or we move our mortgage to another financial institution — to get better terms and a deal that fits our needs more closely.

But why would we want to change the terms at all? There are three main reasons:

First reason for mortgage refinancing (and the most urgent): changes in the household's financial capacity and preferences

Maybe your financial situation has improved, because:

- Your salary has gone up significantly.

- You finished vocational training or a degree and can now command a higher salary.

- You paid off loans and/or obligations that were weighing on your monthly cash flow.

Or maybe it's changed for the worse, because:

- A change in employment led to a drop in salary.

- An illness left you unable to keep up your income.

Either way, it's worth adjusting the monthly payment to match your new cash flow.

If the downturn in your financial situation is expected and planned (say, you already know you'll start a startup, take a long break, or relocate abroad), it's best to refinance before the change — because the financial terms you get depend on your current financial data.

Another reason to refinance is to change your resource allocation — that is, how you split your money among obligations (loans), investments, and day-to-day expenses.

Second reason for mortgage refinancing: rates are now lower / you can build a better mortgage

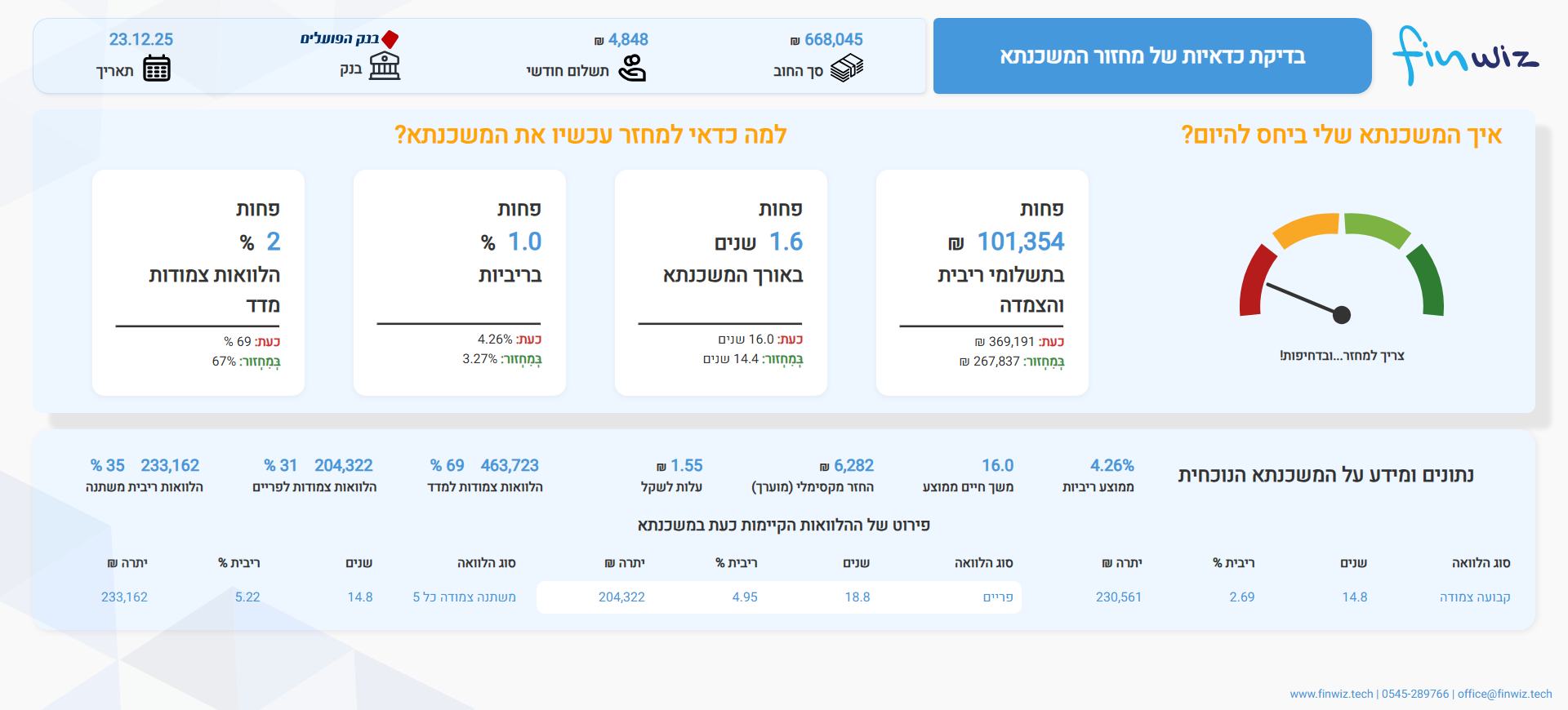

There are three ways to tell whether refinancing is worthwhile:The first (and easiest) way to check whether refinancing is worthwhile: analyze your mortgage with our system and find out whether it can be improved

Instead of getting bogged down interpreting the data yourself (as we'll describe in the next two methods), you can simply let us do the work. Go ahead and download a loan payoff statement from your bank's website and submit it for analysis through our system. You'll quickly get an analysis of where things stand and what you can achieve or improve at the same monthly payment and risk level. Alternatively, you can take a first crack at it yourself with our mortgage calculator and build a new mortgage mixture before refinancing.

The second way to check whether refinancing is worthwhile: check whether current mortgage rates are lower than yours

It's worth refinancing if current mortgage rates are lower than the rates on your mortgage. You can see the current rates here.

Suppose you have a loan with 20 years left, and looking at the current rates you see that most people are getting lower rates on the same loan for the same term — that's a sign it's worth calling your bank and exploring whether you can bring the cost of the loan down.

The third way to check whether refinancing is worthwhile: examining the size of the early prepayment fee in the loan payoff statement

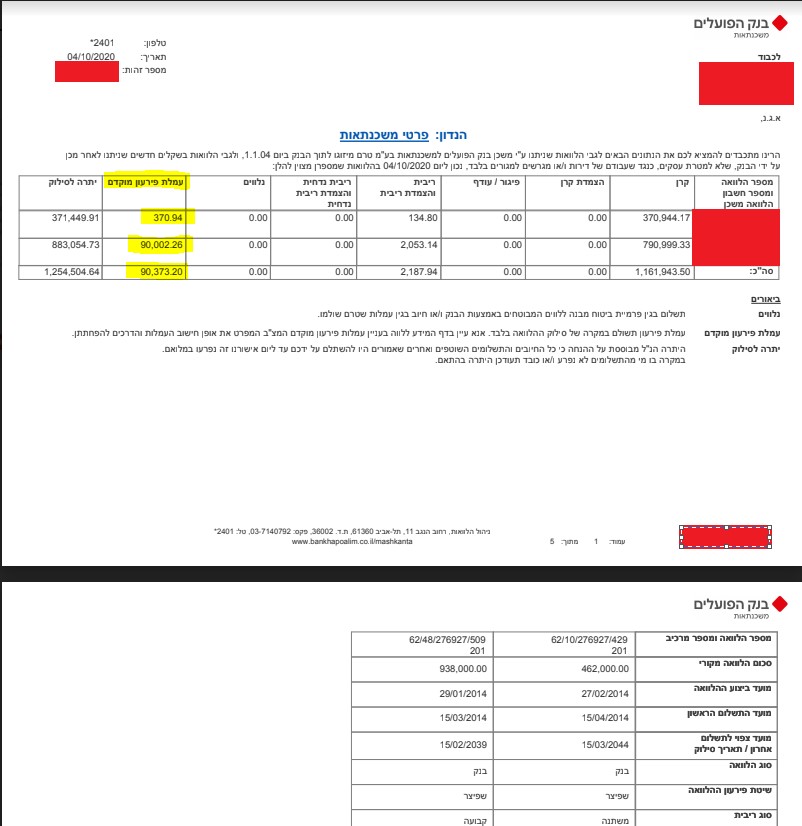

A PDF document the banks produce, meant to give you everything you need to weigh up refinancing.

It lays out your existing loans, the remaining payments, the outstanding balance, whether there's an early prepayment fee, and so on.

The key number for judging whether refinancing is worthwhile is the size of the early prepayment fee (which some banks call the discounting fee or discounting differential).

We've attached an example of such a statement from Bank Hapoalim. The first page lists all the loans in the mortgage, and for each one it states the size of its early prepayment fee.

You can see that the fee is roughly 90,000 NIS. Our rule of thumb: when the early prepayment fee tops 10,000 NIS, refinancing is usually worth it. The reason there's a minimum threshold at all is that refinancing comes with extra overhead costs (described later) that eat into the benefit.

The method above is only partial, because it's blind to loans that carry no early prepayment fee — such as the prime-linked track and a euro-linked loan.

In practice, this approach is most useful for checking whether the terms on your fixed-rate tracks are good, or whether they need refinancing.

That said, there are cases where the fee is below 10,000 NIS but refinancing is still justified. The most common one involves reductions to the early prepayment fee.

The Banking Ordinance defines time periods that grant a discount on the size of the early prepayment fee. These time periods are described in Section 8 of the Banking Ordinance (Early Repayment of Housing Loans) - 2002.

Very (very!) roughly, after a certain period (say, three years) a discount kicks in on the early prepayment fee. So you might have a high fee — a sign that refinancing is worthwhile — but the discount drops it below the threshold we'd call "worth refinancing."

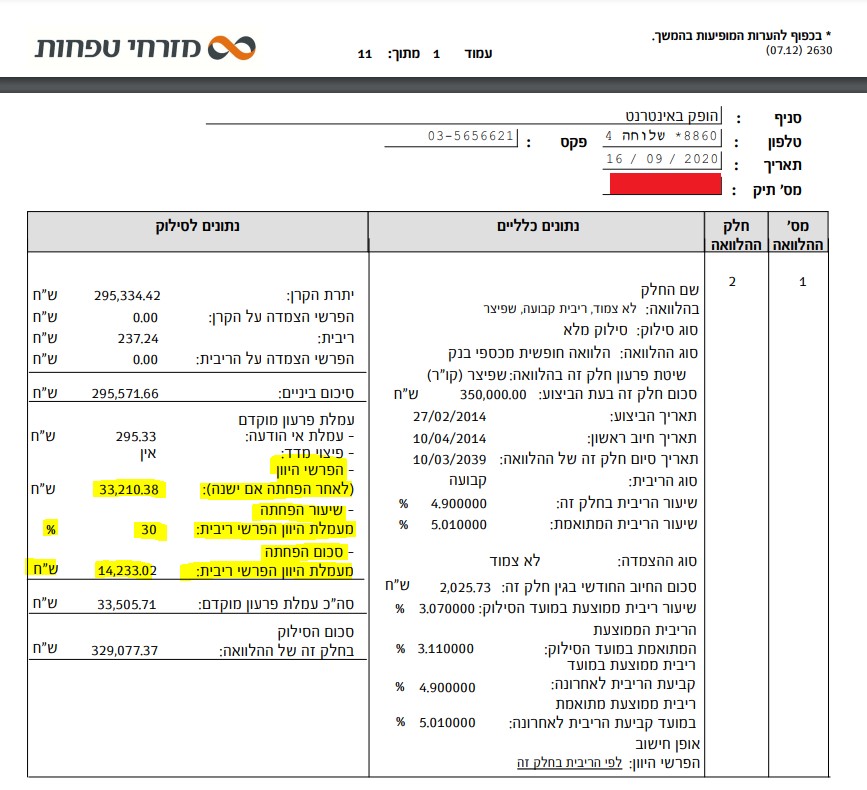

Looking at an example of a loan payoff statement from Mizrahi Tefahot Bank, we can see that this borrower had an early prepayment fee of 47,443 NIS, and thanks to 30% reductions, the final fee dropped to 33,210 NIS.

In the calculator we developed for you, you can calculate the early prepayment fee for each of the cases discussed here

Third reason for mortgage refinancing: the property value has risen and the LTV bracket has dropped

Suppose the property is worth more today than it was when the mortgage was taken out. As a result, the LTV (the ratio between the loan amount and the property value) has dropped into a lower bracket — and you have the option of refinancing the mortgage and benefiting from lower interest rates.

Israel uses three LTV brackets:

- The lowest bracket applies when the LTV is below 45%.

- The middle bracket applies when the LTV is above 45% and up to 60%.

- The highest bracket, with the highest interest rates, is above 60% of the property value.

First example: if the property is worth one million NIS and the mortgage is 400,000 NIS (40% LTV), we're in the lowest interest rate bracket.

Second example: if we take a mortgage of 750,000 NIS on a property worth one million NIS (75% LTV), we're in the highest interest rate bracket.

Changing the LTV bracket: suppose that after construction is complete, the property in example two rises to 1.25 million NIS. Now 750,000 NIS is 60% of that 1.25 million — and we've dropped to the middle LTV bracket.

Even with the drop in LTV bracket, refinancing isn't necessarily worth it. If rates are higher at the time of refinancing than they were when you took out the mortgage, refinancing doesn't pay off. You can read about the gamble involved in planning for future refinancing

Step two: How to plan the mortgage refinancing

We've established that we need to refinance, and that it's worth changing things. So how do we change the deal? What exactly needs to change?

First step: What do we want to achieve?

Let's split the task in two. First, we need to figure out whether the mortgage mixture needs to change. Does the mixture we chose back then still suit our needs today? Is our monthly payment still right for us?

If the current mortgage mixture still suits our needs, the task gets simpler. We just approach the banks and negotiate the interest rates, exactly as we did when we first signed the mortgage, to land the cheapest offer.

If, on the other hand, the current mixture no longer fits our needs, we'll need to plan a new one. We can head back to the Knowledge Center or opt for mortgage advisory services (we'd be very happy to help).

Second step: Who do we do this with?

We've settled on a mortgage mixture; now we need to find the bank that will give us that mixture for the lowest monthly payment. We have two ways to get there.

We can refinance the mortgage at the bank where it's currently held. This is called internal refinancing.

The advantage of internal refinancing is that it skips a lot of the bureaucracy (described later), so it's simpler and faster. The downside is that the bank knows you're a "captive" customer and won't offer you its best interest rates.

💡Background: why would our bank give us better interest rates at all?

Why would our bank agree to lower the interest rates on the mortgage at all? After all, we struck a deal with the bank in the past. Reopening that deal and improving our rates would hurt the bank's profitability — and it's under no obligation to agree. The answer lies in the market spread.

Let's illustrate with an example from John Doe's mortgage. First, a reminder: the basis for pricing mortgage rates on fixed and variable loans is the yield on Israeli government bonds.

John Doe took out a mortgage in December 2018 — the green circle in the image below. For the sake of simplicity, say that at the time the anchor-rate (or basis) for pricing the loan he requested was 2.36% (we pulled it from the chart). On top of this basis, the bank added its market spread, and that's how the final rate was set.

Israeli Government Bond Yield for a 10-Year Term as a Function of Time

A year later, John Doe decided to refinance. He saw that interest rates had fallen significantly. By the time he refinanced, the anchor-rate for pricing the loan had dropped to 1.02% — 1.34% below the original anchor. This is the green point in the image above. On the new anchor, the bank added the same market spread, so the final rate came down.

In refinancing, the bank closes the old loan and opens a new one with exactly the same profitability as before. So where does its profit come from? John Doe had 14,000 NIS in early prepayment fees — which were rolled into the new loan he opened — and on top of that, the bank charged an operational fee.

With external refinancing, by contrast, we negotiate with other banks.

If the banks do want to sell us a new mortgage, we can negotiate our way to better interest rates and terms. The catch is that external refinancing comes with more bureaucracy — you have to go through a fresh collateral process (property appraisal, mortgage registration, life insurance, and so on).

Step three: In practice - how to refinance the mortgage

External refinancing works much like taking out a new mortgage. We prepare documents and negotiate with the banks over the optimal mortgage mixture we built. Once we're down to the bank with the lowest offer, the stage of moving the mortgage out of one bank and into another begins.

First, we ask the bank where our mortgage is held — the one we're moving it away from (let's call it the "old bank" for simplicity) — for a letter of intent.

The bank declares that if it receives the full mortgage amount by a certain date (this is the validity period of the letter of intent), it will remove the collateral pledge from the seller's property.

We present this letter to the bank we're moving the mortgage to (let's call it the "new bank"). Before the new bank agrees to hand over the money, it'll want to protect its investment, so it submits a request to register a second-degree mortgage. The new bank wants to be the mortgagee bank, but since we still owe the old bank, the new bank gets registered as the second-priority mortgagee bank.

The new bank is a second-priority creditor. This means that if we become insolvent, the property is sold, and the first-priority creditor (the old bank) is entitled to the sale proceeds first — to cover what you owe it. If any money is left over, it goes toward the debt you owe the new bank (the second creditor).

Once the old bank consents to the second-degree pledge, we register a second-degree mortgage in favor of the new bank.

We'll also need to take out additional life insurance on the mortgage at the new bank. The reason we end up with double coverage is that we still owe the old bank, and it will refuse to release the existing life insurance policy. Use our life insurance calculator to compare quotes for the new policy.

And now, once we have the second-degree mortgage registration and life insurance in favor of the new bank, it transfers the money to the old bank. On receiving it, the old bank removes its mortgage and stops being your mortgagee bank.

The final, bureaucratic stage is converting the second-degree mortgage into a first-degree pledge — at which point the new bank becomes our mortgagee bank. You can also cancel the old bank's life insurance policy at this stage. And that's it! We're done.

Nobody at the new bank will chase you to complete the transfer of the pledge from second degree to first degree — but you should know that you're obligated to do it. If you don't, you may run into trouble when you go to sell the property down the line.

We want to stress that this collateral stage is a real hassle — but it shouldn't scare you off refinancing, as long as it makes economic sense.

Good luck.