Don't Count on a Future Rise in Your Property Value

When we carry out a mortgage refinancing, we are asking our bank — or another bank through which we did not originally take the mortgage — to change the structure and terms of our mortgage. We can change the entire mortgage mixture from top to bottom, or in the simpler case, simply request that the interest rates in the mixture be updated to reflect current market conditions. This is an excellent way to reduce the cost of the mortgage and allows us to adapt it to the changing needs of the family.

A reminder about interest rates

At earlier stages, we told you that there is a connection between the LTV (loan-to-value) and the level of interest rates you receive. The LTV is how much money we borrowed from the bank.

- Below 45% financing: the best interest rates

- Between 45% and 60% financing: intermediate rates

- Above 60% financing: the least favorable rates

As a reminder: in a mortgage, what matters is not the interest rate itself but the market spread (which directly affects the interest rates). Each drop in an LTV bracket causes a reduction of approximately 0.1%–0.15% in the market spread, which directly translates into lower interest rates from the bank.

In other words, if you dropped from a 60% LTV bracket to a 45% bracket, you can expect a reduction of approximately 0.15% in the interest rates you receive on your mortgage mixture.

During the period between 2024 and 2025, due to a decline in mortgage demand, banks compressed the market-spread differential between the various LTV brackets to nearly zero.

We want to show how it is (ostensibly) possible to count on a future improvement in interest rates.

Example: purchasing a home from a developer

Suppose we bought a property for one million NIS and needed 700,000 NIS in mortgage financing. We are at 70% LTV — the highest LTV bracket. Two years later, upon completion of construction, the property is worth 1.3 million NIS and our outstanding debt is 670,000 NIS. We are now at 51.5% LTV — we have dropped an LTV bracket!

Based on this example, we can approach the mortgage banks, tell them that our outstanding debt is 51.5% LTV, and that we are in the middle LTV bracket. We can then receive interest rates that are 0.1%–0.15% lower than the rates we had two years ago — when we were in the highest LTV bracket.

This works in theory, but in practice it is somewhat less precise.

Financing mistake: taking out a mortgage from the bank today with the knowledge that you will refinance once construction of the property is complete.

A mortgage mixture with a known and imminent expiry date is entirely different from a mortgage mixture meant to last for many years. If the intention to refinance in the near future is already known, the right approach is to prioritize lower interest rates over hedging risk — this is exactly the bank's standard mixture. The question is whether you understand the risk you are taking.

Why it would be a mistake to plan a future mortgage refinancing

We will now describe three reasons that explain why planning a future refinancing is a mistake.

First reason: gambling on market conditions when carrying out a future mortgage refinancing

For this exercise (a near-certain refinancing in the very near future) to be both profitable and worthwhile, the level of interest rates at the time of refinancing must be equal to or lower than the level of interest rates at the time the mortgage was taken. Interest rate levels change on a day-to-day basis and are linked to changes in the capital markets (more specifically, to changes in Israeli government bonds traded on the Tel Aviv Stock Exchange) — and that is the problem here. If, at the time construction is complete and the moment arrives to refinance the mortgage, the level of interest rates rises by at least the gap between LTV brackets, then all the savings and potential gain evaporate. This is because the interest rates in the lower LTV bracket will be identical to the rates you took when you originally borrowed.

In other words: executing this plan means gambling on the level of interest rates in the near future, when construction of the property will be completed.

Let's look at the interest rates page. Note the historical data for five-year real and nominal government bond anchors — how volatile and erratic they are. There are quite a few months in which the rate is 0.2% higher than in the following month. We remind you that the figures in those charts are the basis for pricing your loan costs — further reading on this is available in the description of the market spread.

If you are unable to refinance — because it will not make sense to do so given market conditions — the result will be remaining stuck with a mortgage that does not suit you or your needs.

By the way, you must also take into account that at the time of a future refinancing you may be required to pay additional costs (who guarantees you will refinance at the same bank?): an additional property appraisal, account-opening fees, power of attorney, early prepayment fees, and so on.

Second reason: your bank is not permitted to recognize the increase in the property value

Yes, you understood correctly. Your property is worth one million NIS more today? Your bank, where the mortgage currently sits, is not necessarily interested. The bank is not supposed to recalculate the payment-to-income ratio.

Let's say the bank decided to recalculate anyway? It makes no difference. The Bank of Israel defines this explicitly — even if the bank independently decides to recalculate the payment-to-income ratio and it goes down, it is prohibited from granting capital concessions. Bank of Israel Q&A — section 6.5.

Although a bank is officially prohibited from recognizing an increase in the property value for the purpose of capital concessions, it may sometimes choose to offer better interest rates at its own internal discretion — but there is no commitment or guarantee that this will actually happen.

So some of you are surely saying now: "No problem, we will do an external refinancing" — well, you will soon see that this door is not really open either.

Third reason: interest rates on an external refinancing may be higher

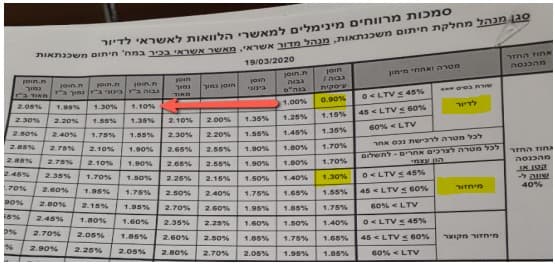

Banks may offer higher interest rates when it comes to a refinancing. We present an internal Bank Hapoalim document — a rate table as a function of the loan purpose and loan characteristics. You can see the level of profitability that banks can approve, as a function of LTV, purpose, and approving authority. Look at the two highlights — you will see that the spread for a refinancing is 0.4% higher than the spread for a regular loan:

Why are they higher? Because they reflect the additional operational cost involved in a refinancing. You need to carry out an additional series of collateral pledges, request a letter of intent from the bank, deal with the mortgagee bank's tactics to keep the mortgage with them (and there are quite a few of those) — so the banks aren't always eager to refinance, and that shows up in the interest rates.

What you should do instead

Do not count on a future mortgage refinancing. The mortgage you take now should be structured to suit your future needs. If in two years' time financing conditions allow for a worthwhile refinancing — you've come out ahead. You can then negotiate, refinance, and benefit from the rise in the property's value. If financing conditions change for the worse — pat yourself on the back: you locked in low interest rates and built a mortgage that suits your needs for years to come. Well done!

To build a mortgage mixture that works from day one, use the mortgage calculator and see exactly what the monthly payment and total cost will be.

Good luck!