Why you should not shorten the term of the fixed-rate loans in the mortgage mixture

An unbalanced mortgage mixture is very common among mortgage professionals and borrowers alike. It's the mortgage bankers' default mixture, and it's also caught on with some mortgage brokers and some amateur mortgage planners on the various forums.

Why does this structure exist, and why is it so widespread? Roughly speaking, the loans banks offer fall into two types:

| Loan type | Effect on the interest rate when extending the term | Effect on the interest rate when shortening the term |

|---|---|---|

| Fixed-rate loans ( KALATZ, KATZ, ZAKAOT) | The interest rate rises | The interest rate falls |

| Variable-rate loans ( MALATZ, MATZ, prime-linked) | The interest rate is not affected | The interest rate is not affected |

We will extend the loan duration as much as possible for the variable rate loans, whose interest rate does not depend on the loan duration.

We do this to reduce the monthly payment — the longer the loan duration, the lower its monthly payment.

With the freed-up funds, we will shorten the loan duration of the first type of loans, thereby reducing their interest rate.

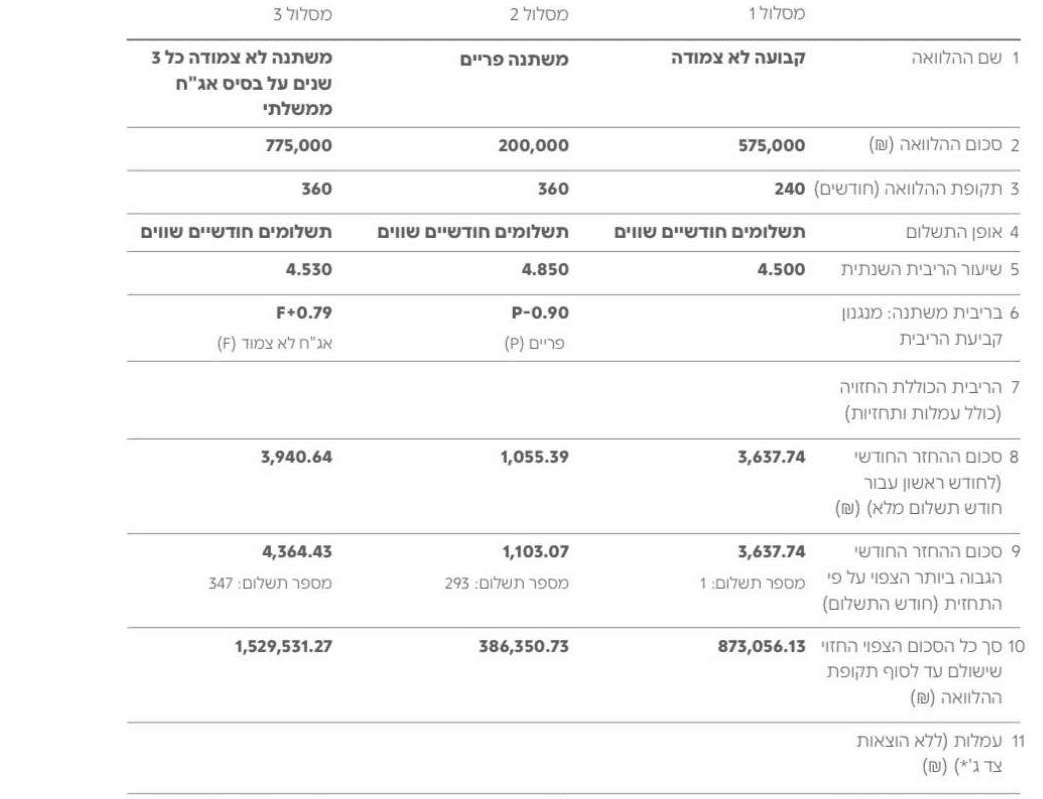

Take a look at this example of such a mortgage mixture from Bank Hapoalim. The prime-linked and variable-rate loans were stretched to 30 years, and the term of the fixed-rate loan was cut to the shortest possible (subject to the desired monthly payment).

The appeal of this structure is obvious. For the same monthly payment, we get lower interest rates. On top of that, the short loan plants a psychological "milestone" in the near term — we'll feel like we've made real progress on the mortgage once that loan is paid off. And finally, we're convinced that when the short loan ends, we'll raise the payment on the longer loans and shorten them.

But we also want to lay out the downsides of this structure. We'll show why it's an expensive, risky mortgage mixture, and why you should think twice before choosing it. That doesn't mean it's never the right call. If your mortgage runs for a short period after which it will definitely be refinanced, and you also expect inflation, the prime rate, and Israeli Government bonds to stay at their current low levels throughout that period, this could be the right mortgage mixture for you.

By the end of this article, you may be wondering: "if not an unbalanced mortgage mixture, then what?" It would be a mistake to assume that a mortgage mixture where all the loan terms are identical (say, every loan running fifteen years) is the right one. It isn't — it's needlessly expensive.

You get the optimal mortgage mixture by optimizing the repayment ratio. In the optimal mortgage mixture, the loan terms usually won't be identical — but the gap in years won't be very large either. We'll dig into this further in reason number 7 later in this article.

A review of the drawbacks of an unbalanced mortgage mixture

First reason: In practice, the loan term does affect the interest rate

In practice, the loans can be affected by the term. In other words, banks may charge a higher interest rate when you extend a loan's term. Why? It comes down to the banks' risk management.

From the banks' point of view — and to some extent fairly — a longer loan is riskier and so should carry a bigger "premium" or "compensation." For example, one bank bumps up the bank margin on the entire mortgage mixture when the prime-linked loan runs longer than 20 years. At other banks, there's one minimum prime-rate range for one loan term and a different, higher minimum range for a longer term.

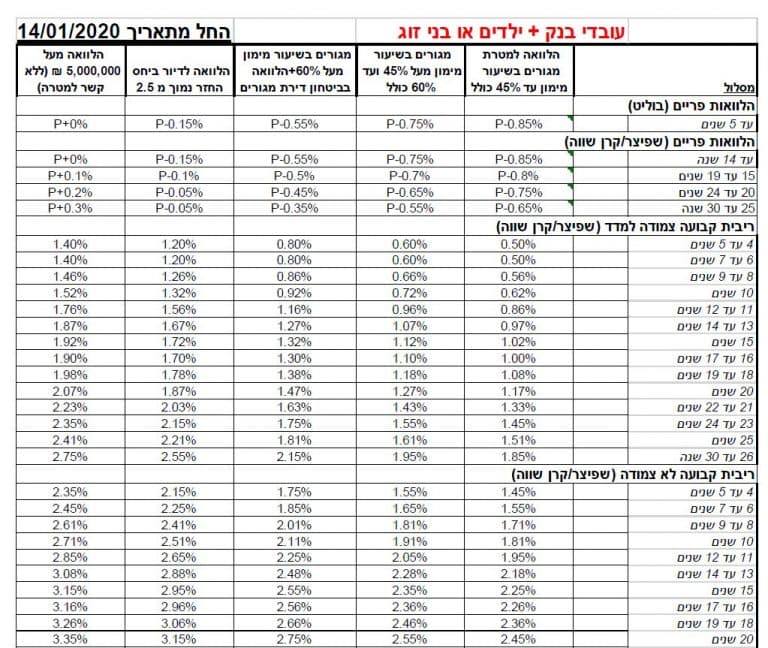

You can see this in the terms bank employees get when they take out a mortgage, or in the terms for customers in large group projects (usually a "chevra" — group deal), where the group negotiates uniform financing terms on everyone's behalf. When they go to take out a mortgage, their bank gives them a document laying out the expected interest rates for each loan track.

Second reason: Regulatory difficulty - you cannot easily increase your payment

Fans of the unbalanced mortgage mixture argue that once the short loan ends, they'll use the freed-up monthly payment to make early prepayments on the variable-rate loans in the mixture. Unfortunately, regulation doesn't allow it. Section 13 of the Banking Ordinance-1941 sets the minimum early prepayment at 10% of the original loan amount, or 10% of the current principal plus interest and CPI linkage differentials — whichever is higher!

If you have to build up the required amount over several months, you'll be paying unnecessary interest and CPI-linkage payments.

Third reason: Want to increase your payment through refinancing? That has its own difficulties and drawbacks

The surefire way to raise your monthly payment is through internal refinancing of the mortgage at the same bank — that is, agreeing with your bank on new mortgage terms. But then you're at the mercy of the bank's willingness and its terms at the time, and just as importantly, the interest rates in effect when you refinance, since the new loan's terms will be set by those rates.

In a refinancing, the bank can offer whatever rates it wants. The data tells us that in an internal refinancing (refinancing the mortgage within the same bank) the rates run higher than in an external one. The bank knows these are captive customers, and it prices accordingly.

Fourth reason: Behavioral economics suggests that in practice we won't increase the payment

The plan looks great on paper: "When the short loan ends, we'll just use the freed-up amount to raise the monthly payment." In reality, life is unpredictable and that doesn't always happen. When the time comes, new needs and wants suddenly crop up — replacing a car, renovating the house, vacations, helping the kids, and more.

We've already explained why this is a problem — we wrote about it in the article on taking short loans from the bank.

Fifth reason: From a risk hedging perspective, the longer we extend the loans - the riskier they become

In an unbalanced mortgage mixture, the loans that typically get extended are precisely the ones driven by external factors. Remember: the longer you stretch a loan, the lower its monthly payment. Since the interest has to be paid, the amount left over to repay the principal (your debt to the bank) keeps shrinking. In other words, a longer loan is one where the principal comes down more slowly.

The upshot is that when the loan's interest rate changes, a larger chunk of the principal absorbs that change. So a significant portion of the loan gets more expensive — and the mortgage as a whole along with it. An unbalanced mortgage mixture puts too much weight on the safe fixed-rate loans, which carry no risk, and therefore too little on the unstable ones, pushing the risk of the mortgage portfolio even higher.

The way to cut risk in the mortgage portfolio is to shorten the term of the risky loans — not extend them.

Sixth reason: Mathematically, this is a more expensive mortgage mixture

We have a fixed, limited monthly payment budget that has to service every loan in the mortgage mixture. If we spend a big chunk of that budget to shorten the term of one loan, it necessarily comes at the expense of the others, which we'll have to extend, making them more expensive. In other words, shortening and cheapening one loan lengthens and inflates another.

Let's use the following example to drive the point home

- A mortgage of 600,000 NIS

- Desired monthly payment: 4,000 NIS/month

- A mixture consisting of 400,000 NIS KALATZ and 200,000 NIS prime-linked

- Interest rate considerations:

- The prime rate doesn't change over the years - it stays at 5%

- The fixed unlinked (KALATZ) rate starts at 4.2% for a 6-year loan and rises by 0.0025% per year.

Interest Rate as a Function of Loan Duration

Here's the first chart — the loan's monthly payment chart. It has three curves. The first (orange) shows the monthly payment for borrowing 400,000 NIS in a fixed unlinked track as a function of the loan term. The second (blue) shows the monthly payment for borrowing 200,000 NIS in the prime-linked track, again as a function of the loan term.

Monthly Payment Curve — Prime-Linked vs Fixed Unlinked

The horizontal red line marks the monthly payment (4,000 NIS) we planned for the mortgage and can't go above. So the mortgage mixture can be built in several ways. For example:

- Take the prime-linked loan for thirty years (monthly payment of 1,073 NIS) and the KALATZ for 16 years (2,915 NIS per month).

- Or you could take the prime-linked loan for 22 years (monthly payment of 1,250 NIS) and the fixed unlinked loan for 18 years (monthly payment of 2,705 NIS).

Notice the slope of the curves in an annuity amortization schedule. It's not linear but exponential. Shortening a loan from 30 years to 27 isn't the same as shortening one from 17 years to 14 — the latter takes far more money and resources.

Now let's turn to the other chart, which shows the mortgage's cost curve. This curve plots the loan's repayment ratio as a function of its term. You can see that the longer the loan, the more expensive it is.

This curve is also exponential, but in the opposite direction — meaning shortening the term from 30 to 27 years has a bigger effect on the repayment ratio than shortening it from 17 to 14 years.

Total Cost as a Function of Loan Duration

Putting all this together, we want to find two points (each representing a different loan term in months) on the cost-and-payment curve — one for the prime-linked track and one for the KALATZ — that meet the monthly payment constraints and minimize the repayment ratio. In engineering terms, that's solving a constrained optimization problem.

Mortgage Mixture Optimization Simulation

Without diving deeper into the math, these curves point to a solution that minimizes the repayment ratio: if we extend the KALATZ (the short one) by a few years, a meaningful amount of money frees up in the monthly payment with only a small effect on the repayment ratio. We then use that freed-up money to shorten the prime-linked track substantially (because over long terms, trimming a few years doesn't require much of an increase in the payment). Cutting a few years off there sharply lowers the repayment ratio on that track, and the overall repayment ratio — a weighted average across all tracks based on their weight in the mortgage mixture — comes down.

The Mortgage Mixture Optimization Process

Starting with an Unbalanced Mixture

Starting point: long prime-linked, short fixed unlinked (KALATZ)

Extending the Fixed Unlinked (KALATZ)

Shortening the Prime-Linked Track

Result: A cheaper mixture at the same monthly payment

Building a real mortgage mixture means finding the optimal mixture across dozens of constraints and thousands of such curves at once. This problem has closed-form solutions that draw on algorithms from computer science — and that's exactly what the Finwiz system does.

Good luck!