How to Improve Your Mortgage Rates - By Drawing Down Mortgage Funds in Stages

In a large share of purchase transactions, the mortgage funds aren't transferred to the seller all at once, but in installments over time. That's the case for new-build purchases from a developer and for self-build construction, where payments are sometimes tied to the pace of construction, and also for second-hand home purchases, where the mortgage funds are sometimes released against various payment milestones (for example, paying off the existing mortgage, or the actual handover of the home to the buyers).

When the gap between one drawdown and the next is large — longer than the rate-lock period (24 days from the last approval) — the question becomes how to release the funds: which loan track from the mortgage mixture to draw now, and which to leave for later stages.

This article tackles that question — the considerations to weigh when choosing a drawdown policy. As we'll explain in a moment, it's a complicated issue with a good deal of guesswork involved, but if you guess right, you can actually end up with better interest rates than the ones you locked in with the bank.

Wait — how is that possible? How can the rates you signed with the bank actually change?

What did we actually negotiate with the bank?

If you negotiated with the bank (and we really hope you did, because most borrowers don't), and you managed to push your mortgage interest rates down at every stage, you need to know that you weren't negotiating over your mortgage rates at all — you were negotiating over the market spread.

In brief: the market spread is the difference between the bank's funding cost (usually Israeli Government bonds, traded daily on the Tel Aviv Stock Exchange (TASE), or the Bank of Israel interest rate).

Every time the bank gave you a better principle approval, it was really cutting its spread — or put more simply, how much it makes on your mortgage.

From the moment the negotiation ended and you signed the mortgage documents, the bank locks in its offer and commits to this spread plan. What does that actually mean?

It means the bank agrees to extend you a "credit facility" with a dynamic cost. That is, whenever you choose to draw funds (after the principle approval period has expired), the interest rate on the money you transfer moves with an objective economic indicator the bank can't influence. That indicator is called the anchor-rate.

At each drawdown, the bank takes the current anchor-rate, adds the agreed spread, and that's the interest rate on the loan.

Illustrating the spread and anchor mechanism

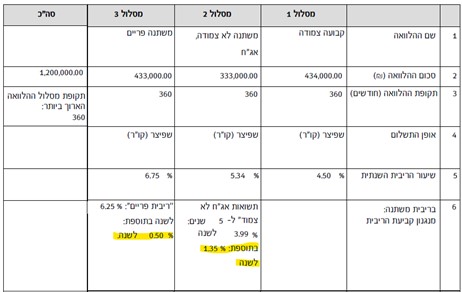

To illustrate how fund drawdowns work, take a look at this first example, from Mizrahi Tefahot Bank:

On the unlinked loans (loan number 2), the bank expects to earn roughly 1.35% above the nominal anchor-rate, and on the prime-linked track (track 3), it expects to earn 0.5% above the prime-linked rate.

Track number 1 is a fixed CPI-linked loan; it too has an anchor-rate, which is spelled out later in the Mizrahi Tefahot Bank principle approval.

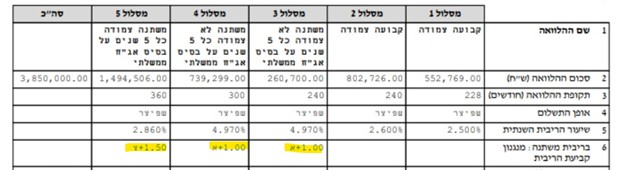

Here is a second example, from Bank Leumi:

In this example, for tracks 3, 4, and 5, the bank spells out the profit it expects on each track in the mortgage mixture. On the unlinked loans (tracks 3 and 4) it wants to earn 1% above the nominal anchor-rate (usually the non-CPI-linked Israeli Government bonds), and on the CPI-linked loans (track 5) it wants to earn 1.5% above the real anchor-rate (usually the CPI-linked Israeli Government bonds).

The fixed-rate loans (tracks 1 and 2) also carry a rate that can change (even though it isn't spelled out as clearly as in the Mizrahi documents), as you can see in the Bank Leumi documents:

📚Background: this isn't fair — we signed with the bank on set rates, so why is it suddenly changing them?

When the bank commits to giving us a mortgage, it has to source and reserve the amount it promised us — out of its profits, its customers' deposits, or some other way. But here's the key point: on that money, now reserved for us, the bank has to pay from the very first moment it ties it up. It either pays interest to whoever supplied the money, or it simply earns nothing on it because it can't put it toward other profitable activities.

If the bank parked unused funds (reserved for us but not yet drawn), it would lose money. So instead it commits to extending the credit facility we talked about. Each time we request another installment, it raises the money from its sources at that moment and hands it over on the terms we signed.

What to do to receive better interest rates

Now that we understand how mortgage interest rates get set, we need to plan the transfer of funds carefully — deciding how much to transfer and when.

First, two important points to flag:

- Bank of Israel policy: at every stage we must comply with Bank of Israel regulations and limits. The main emphasis is that at any given moment, at least 33% of the amount drawn from the mortgage facility to date must be in fixed-rate loans (a fixed unlinked loan, fixed CPI-linked, or a government-subsidized mortgage).

- Some loans can't be locked in: for the prime-linked loan and loans linked to the euro or dollar, the timing of the drawdown makes no difference. Whether you draw the funds in a month, two months, a year, or even sooner, you can't influence the interest rate at all. If you drew the money when the prime-linked rate was low and it has since changed, your monthly payment changes accordingly. For this reason, we recommend leaving these amounts for the last drawdowns.

Now for the practical tips: the yield and price of Israeli Government bonds are what drive the interest rate on the mortgage tracks (both the variable-rate and the fixed-rate loans). Since predicting the future price of Israeli Government bonds is extremely hard — and we probably have no real experience at it either — we'll try to predict something we maybe understand a little better (at least from Friday-night living-room debates): the macroeconomic situation of the State of Israel. Remember we told you this involves a bet?

Israeli Government bonds reflect the political and economic state of the country — that is, how the market sees the opportunities and risks Israel has to contend with. If Israel shows financial resilience and sound economic management, the price of these bonds rises, and mortgage rates fall as a result. Conversely, if Israel faces economic challenges and/or is poorly run, the price of the bonds falls, and mortgage rates rise.

We need to decide whether we're optimistic or pessimistic about Israel over the stretch of time when we'll be releasing money to the seller. Let's go through what to do in each scenario.

How to release the funds if we think Israel's macroeconomic situation will worsen in the near term:

If we think Israel's macroeconomic situation is going to deteriorate in the near term, that means we expect interest rates to rise above their current level. In that case, here's what to do:

- Draw as much of the mortgage funds as possible now — that's how you lock in rates before they rise. Any funds you don't draw now are exposed to increases in Israeli Government bond yields, and so will get more expensive. It's worth stressing that this can create legal risk for you (since you have no protection once you've transferred the excess money to the seller) and/or cash-flow risk (drawing more money than planned right now can push you into overdraft).

- In order to minimize a future early prepayment fee: draw the fixed-rate loans first, not the variable-rate ones. Because fixed-rate loans carry a higher prepayment fee than variable-rate ones, drawing them first gets you better rates on them — which lowers the future early prepayment fee.

- If our mortgage mixture includes a teaser-rate loan / tracks intended for future prepayment / balloon loans: draw those last (as much as you can). These are loans you won't be keeping for the long term, so their interest rate matters less than locking in the rates on the loans you'll keep for years. The same goes for loans whose rate can't be locked in, like the prime-linked loan or foreign-currency-linked loans.

How to release the funds if we think Israel's macroeconomic situation will improve in the near term:

If we think Israel's macroeconomic situation is going to improve in the near term, that means interest rates are going to fall below their current level. In that case, do the following — which is exactly the opposite of what we described above:

- Draw as little as possible now. Funds you don't draw now are exposed to a fall in Israeli Government bond yields, so their interest rate gets cheaper. For new-build purchases from a developer, this strategy has a drawback — increased exposure to the Construction Input Price Index (CIPI).

- To minimize a future early prepayment fee: draw the variable-rate loans first rather than the fixed-rate ones (though, to meet the Bank of Israel requirement, at least a third of what you transfer must still be in fixed-rate loans). Because fixed-rate loans carry a higher prepayment fee than variable-rate ones, drawing the variable-rate loans first means you'll (on our assumption) get better rates on the fixed-rate loans later — lowering the future early prepayment fee.

- If our mortgage mixture includes a teaser-rate loan / tracks intended for future prepayment / balloon loans / loans whose rate can't be locked in (prime-linked or foreign-currency-linked loans): draw those first (as much as you can). These are loans we won't be keeping for the long term, and we want to buy "time" for bond prices to fall so we get better rates on the loans we are keeping.

Mortgage drawdown planning

The tool below lets you plan your mortgage drawdowns in the best possible way. Enter your mortgage details, including the loan tracks, amounts, and interest rates, then set the drawdown dates and the amounts you want to draw in each installment.

It'll help you confirm that each drawdown meets the Bank of Israel's drawdown conditions. You'll also see how each drawdown changes your monthly payment.

Want to plan the full mortgage and see what the amortization schedule looks like? Go to the mortgage calculator.

Good luck!