The Teaser-Rate Loan — How to Get Better Interest Rates

Almost any method is legitimate when the goal is to reduce the cost of a mortgage. We reconnect with mom's uncle who used to work at a bank in order to get special benefits, we approach mortgage bankers at five different banks to get competitive offers. We might even transfer our checking account if we can shave a fraction of a percent off some track. The methods above refer to actions taken during negotiation. By contrast, there are actions you can take during the mortgage mixture planning stage to achieve further savings on the cost of the mortgage. The most common method is called the "teaser-rate loan."

This article reviews the benefit of executing a teaser-rate loan, how to plan and carry it out, and finally discusses the conditions under which it is actually worthwhile. The most important part of this article is the last two paragraphs - and if you don't have the energy to read 1,500 words, skip straight to the end.

This article also applies to any other savings technique where we choose, right after taking out the mortgage, to pay down chunks of it and thereby shrink it and bring its cost down.

What is the teaser-rate loan? How can it be used to reduce the mortgage cost?

In the teaser-rate loan, we ask to borrow an amount of money that is higher than what we actually need to take. If, for example, our apartment is worth 1.55 million NIS and we need a mortgage of 690,000 NIS, we ask the bank to lend us a larger amount - for example 790,000 NIS - which is 100,000 NIS more than we originally needed.

Why do we ask to take an amount higher than what we actually need? The answer lies in the profit the bank expects to earn on this transaction - this is the bank margin.

Bank margin - the difference between the mortgage interest rate and the funding cost, net of the bank's operating costs.

For more information, see the article on loan fundamentals.

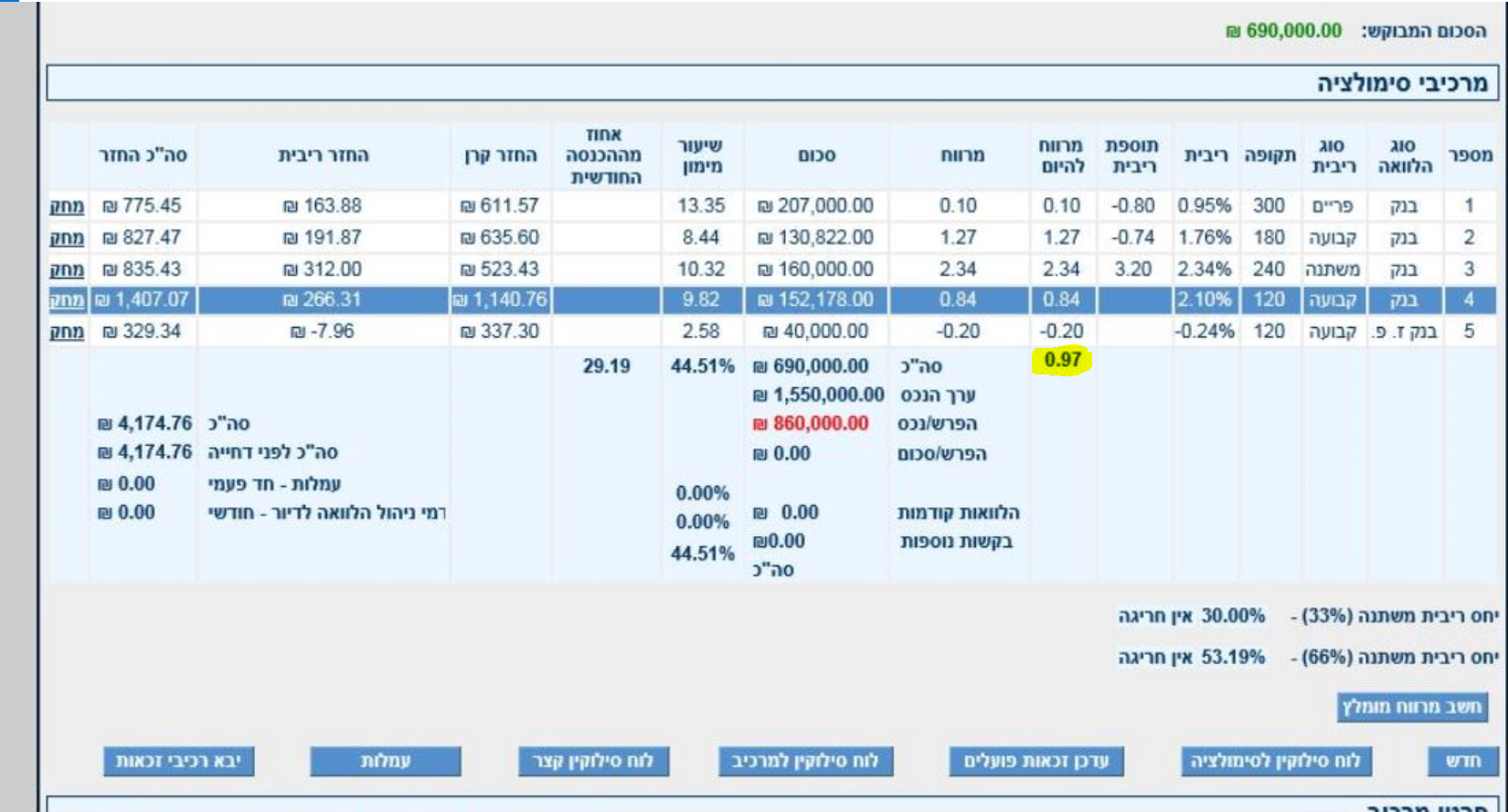

To illustrate this, take a look at the following image:

The number highlighted in yellow, 0.97%, is the expected profit to the bank from granting this mortgage. This number is obtained by calculating a weighted average across all the loans in the mortgage mixture - that is, multiplying the amount of each loan by its spread and dividing by the total mortgage (in this example, 690,000 NIS).

The profitability level is the basis of the transaction. The mortgage banker will set the interest rates in the mortgage mixture in order to meet this number. A drop below the approved number will prevent the deal from being approved. Therefore, if we want to lower the interest rate on one track, we must raise it on another in order to keep the overall profitability level above 0.97%.

An additional insight that emerges is that every loan above 0.97% is a loan that increases the bank's profitability, and every loan below 0.97% is a loan that reduces the bank's profitability.

- Loss-making loans (reduce the bank margin):

- Loan number 1 - spread of 0.1%

- Loan number 4 - spread of 0.84%

- Loan number 5 - spread of 0.2%

- Profitable loans (increase the bank margin):

- Loan number 2 - spread of 1.27%

- Loan number 3 - spread of 2.34%

Now let's return to those 100,000 NIS we described above. Let's assume, for the sake of discussion, that we take those additional 100,000 NIS and add them to the amount we planned to take in loan number 3 - this is a CPI-linked variable-rate loan adjusted every five years. That is, instead of borrowing 160,000 NIS, the loan now stands at 260,000 NIS.

What will happen to the bank margin now? The bank margin will now rise to 1.15%, which is 0.18% above our target margin, and we can therefore now reduce the interest rate on the other tracks until we return to the planned margin of 0.97%.

Back to the basic problem - we borrowed 100,000 NIS that we have no need for. What do we do with them now? Well, after we transfer the full amount to the seller, we can immediately repay those 100,000 NIS and thereby reduce the debt back to the original amount we had planned from the start.

Important! We must not reveal our intention to the bank at any stage. If it knew about the plan to repay the loan immediately, it would neutralize its profitability in the mortgage mixture (that is, treat it as though it does not exist at all).

Interim summary: Thanks to taking an additional and seemingly unnecessary sum of money, we managed to raise the profitability of the entire portfolio, which lets us lower the interest rates on the other tracks — the ones we actually keep.

The savings potential of incorporating a teaser-rate loan into the mortgage mixture

How much money can be saved by incorporating a teaser-rate loan into the mortgage mixture? The savings potential varies from one mortgage mixture to another, depending on the amount borrowed and the interest rates received - so we provide a representative example here.

Let's examine, for example, the mortgage mixture in the image above — without the teaser amount. If we calculate, we will find that the weighted average interest rate is 1.62% and the theoretical cost of the loan (the cost of the loan without any change in the prime rate, the Consumer Price Index (CPI), or the anchor rate) is 1.15 NIS per NIS borrowed - meaning for every NIS borrowed we repay 15 agorot back on top. The estimated cost, which includes expectations for changes in inflation, prime, and the Bank of Israel rate (based on the expectations prevailing at the time of writing) stands at 1.293, which is 202,000 NIS.

Now, let's add those 100,000 NIS to the variable-rate track (loan number 3), as we described earlier. Thanks to the addition, we can now reduce interest rates on the other tracks. We cannot say exactly how much can be reduced because the bank margin on each loan is unknown to us (it is in fact an internal figure of the bank and remains confidential), so we reduced the interest rates to preserve the market spread. For this purpose, we reduced the interest rate on track 2 by 0.16%, the interest rate on track 3 by 0.22%, and the interest rate on track 4 by 0.3%. It is important to emphasize - the reductions could be larger or smaller than this, subject to the bank's constraints.

In the new loan - the weighted average interest rate fell to 1.56% and the theoretical cost (after repaying the teaser amount) fell to 1,120 NIS per 1,000 NIS borrowed. The estimated cost fell to 1.244, which is 193,000 NIS. In other words - we saved 9,000 NIS here!

Sounds great, right? Remember these figures - we will return to them later.

The steps and actions in executing a teaser-rate loan

Let's now understand exactly how to plan and incorporate a teaser-rate loan into the mortgage mixture. First, what will be the size of the addition we take? True, the larger the amount we take - the more we raise the profitability of the portfolio and the better interest rates we get on the other loans. But is there such a thing as "too much money in the teaser-rate loan"?

The answer is yes. There's an amount that's too large, and once we go past it, the whole move stops being worth it. First, if taking the extra amount pushes us across the edge of our LTV bracket into the next one, we'll get higher interest rates on every loan in the mortgage mixture.

Rule one: The amount of money allocated to the teaser-rate loan is, at most, the monetary difference between the LTV at which we want to end up (after repaying the teaser) and the upper edge of the LTV bracket we are currently in.

Let's illustrate with an example. We bought an apartment worth 2,000,000 NIS and planned to take 1,100,000 NIS as a mortgage, which is 55% of the property value. We are in the middle LTV bracket - the one ranging between 45% and 60% financing. If we take more than 100,000 NIS extra we will exceed 60% LTV and move up to the next LTV bracket - meaning our interest rates will rise by an average of 0.1%-0.2%.

Rule two: It is worth examining whether to execute a teaser-rate loan if the payment-to-income ratio (PTI), including the teaser loan, exceeds 35%.

A reminder: every debt we take on, we must service. If we borrowed an additional sum - we must meet the monthly payment on that amount. Suppose, for example, that we want to borrow an additional 100,000 NIS; then the monthly payment will increase by at least 400 NIS per month. Therefore, if our payment-to-income ratio (that is, the ratio between the total mortgage payment and income minus liabilities) exceeds 35% - we risk not getting the deal approved and receiving less attractive interest rates.

Rule three: Choose the CPI-linked variable-rate loan adjusted every five years for the teaser-rate loan.

The way to lower the mortgage mixture interest rates begins with raising the bank margin as aggressively as possible. Therefore, for the teaser-rate loan we choose the loans that are most profitable for the bank. These are the variable-rate loans. For example, the CPI-linked variable-rate loan adjusted every five years is a very good loan for this purpose. Because it is CPI-linked, it has a lower monthly payment than an unlinked variable-rate loan - which will reduce the risk of exceeding the 35% payment-to-income ratio limit mentioned above.

An additional advantage of the variable-rate loan is that the discounting fee / early prepayment fee we are exposed to (if there is one) will be lower than for a fixed-rate loan, because under Section 4 of the Banking Ordinance 2002, the economic loss caused to the bank is discounted only up to the nearest interest rate update point. In the case of a variable-rate loan adjusted every five years - that means five years from the date of taking it out.

Rule four: In order to keep all options open for incorporating a teaser-rate loan - transfer our down payment to the seller up to the upper edge of the LTV bracket we want to be in, and no more.

As stated, in order to incorporate a teaser loan, we will need to borrow more money than we actually planned. For us to actually take this surplus amount, our outstanding balance to the seller must allow for it. That is, if we originally wanted to borrow one million NIS and our outstanding balance to the seller is 1,050,000 NIS, we cannot incorporate a teaser loan of 100,000 NIS - only at most 50,000 NIS.

The costs of using a teaser-rate loan

Incorporating a teaser-rate loan involves paying costs. For example, our life insurance will increase - because it is directly tied to the loan amount we took. Of course, after repaying the teaser loan we will adjust the insurance amount again - and the payment will decrease.

At the time of repayment, we are exposed to fee payments that must also be taken into account:

- Operational fee: totalling 60 NIS.

- No-notice fee: which we can avoid if we give the bank ten days notice before repayment.

- CPI indexation fee: which we can avoid if we repay the loan between the 15th and the 31st of any month.

- Discounting fee: which depends on the difference in interest rates between the date of taking out the loan and the date of repayment. This fee cannot be eliminated.

Is it even worth taking a teaser-rate loan?

When is it worth incorporating a teaser-rate loan? Only after we've settled — following careful thought and a real financial analysis of our liabilities and investments — on the right LTV for us, confirmed that it sits below the edge of the LTV bracket, and checked that we meet the repayment conditions above. What worries us is the cases where people skip the careful thinking and the financial analysis and jump straight to a teaser-rate loan.

Now we get to the part that matters most. First, we want to be clear: we didn't really want to write about the teaser-rate loan at all. We didn't want to raise the profile of this technique — which would only lead to more people misusing it.

The main reason this article was written anyway - following the many cases in which the loan is incorporated into the mortgage mixture automatically and in practice causes the borrower more harm than benefit. We hear from our clients at the opening conversation: "We want you to build us a mortgage mixture with a teaser loan." The heuristic of automatically incorporating a teaser loan is a focus on tactics and "trench warfare" with a complete disregard for strategy and financial planning.

In our approach, the mortgage planning process (as carried out by us during the mortgage advisory process) works as follows:

Those who automatically request to incorporate a teaser-rate loan into the mortgage mixture are skipping the two (more important) steps that come before in the process:

Before we rush to execute a teaser-rate loan, we should stop and understand - is it really right for us to be at 55% LTV, and not at 60%?

What will give us greater economic benefit: being at 60% LTV with 100,000 NIS in income-producing investments, or being at 55% LTV after executing a teaser-rate loan but with no investments?

For those who want to borrow and leverage funds from their study fund (keren hishtalmut) in order to use the money to execute a teaser-rate loan - it is worth stopping and thinking whether this is the best use of the study fund money.

For those who want to redeem their investments in order to "beat the bank" and receive interest rates that are 0.1% lower - yes, you invested 100,000 NIS in the teaser, and you managed to save 50,000 NIS in mortgage interest over the entire loan term. But what could those 100,000 NIS have done for you during that same period?

Is it the right thing to invest money and resources, incorporate a teaser-rate loan, and lower the weighted average interest rate of the mortgage portfolio from 2.3% to 2.1%, when those same resources could have generated an annual return of 5% for us?

The real teaser loan - the lever for economic growth

Let's tell you now what the real teaser loan is in our eyes. The perfect teaser loan in our view is the one that enables us to take money - not for housing but to finance our economic growth goals.

Let's assume, for example, that we want to buy a property for 2,000,000 NIS and decided, after careful thought, that we want to be at 40% LTV. We then ask the bank for another 5% - which is 100,000 NIS. We take it for the maximum term - 30 years. That is a monthly payment of 477 NIS given a 4% annual interest rate.

Those 100,000 NIS are the money that will serve us to purchase real estate in the US that will generate a much higher return.

It is the money with which we can finance the first three months of salary of the first employee in the business, or the purchase of the initial inventory.

It is the money that will serve us for paid advertising in order to grow the clinic we just opened.

It is the money that will give us five months of living expenses - so that we can quit our job and work on our new business.

It is the money that will serve us to carry out the home renovation we have long wanted to do.

Before you rush to take the smallest and cheapest mortgage and then, heaven forbid, find yourself cash-strapped with a loan from the bank or from a study fund for seven years to finance your goals - ask yourself: who fell for the bait? The bank? Or did you fall into the trap of wrong financial planning?

It does not matter at all whether you are salaried or self-employed. Whether you are entrepreneurs or those who actually enjoy the status quo - without thinking about how to use this cheap financing - you will miss out on far more than 9,000 NIS.

The chance to get debt this cheap and this convenient, for this long, only exists through a mortgage. It's a nearly once-in-a-lifetime gift, and our advice is to make sure you don't throw it away for the sake of 9,000 NIS less in interest.

Good luck!