How to Know Which is the Best Offer You Received from the Banks

The longest part of taking out a mortgage (though not the most important) is negotiating the interest rates on your mortgage mixture. We've already described in detail how to run an interest rate tender — that is, how to motivate the mortgage banker to give you the best rates. But before you start negotiating, it's crucial to understand where you actually want to end up. Without a professional mortgage advisor at your side, you'll have to figure out which offer is the best fit for you out of all the ones you receive. As you'll see below, that's no simple task — a mortgage has plenty of variables that determine its quality: initial monthly payment, estimated maximum monthly payment, average interest rate, mortgage duration, repayment ratio, and more.

Mortgage bankers are skilled at reshaping and manipulating the mortgage mixture to give you everything that sounds good — even if the end result is a terrible mortgage. So in this article we'll walk through the right and wrong ways to compare different offers and mixtures, so you know how to pick the right one.

The tool we'll use in this article is the mortgage mixture comparison table. It pulls together all the offers you received over the past month and compares them across a range of quantitative parameters. To see how different mixtures affect your monthly payment and total cost, try our mortgage calculator.

Wrong ways to compare mortgage mixtures

We want to start with what not to do — that is, how not to compare mortgage mixtures. In our experience, a good chunk of the tips floating around on social media, and even among friends and family, is terrible advice. Relying on the heuristics and rules of thumb described below is exactly what can lead you to a bad mortgage. For each method, we'll explain the metric and show how it can be manipulated to make a mixture look better than it really is.

❌Wrong method #1: Comparing by the lowest weighted average interest rate

The first method is using the weighted average interest rate. Because it's such a flawed basis for comparison, this parameter isn't even shown in the mixture comparison table. Still, since we've run into it before, it's worth addressing.

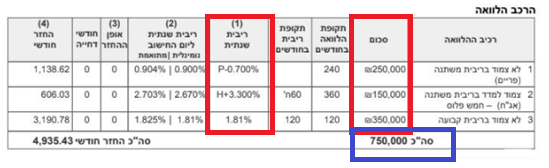

First, a quick explanation: the weighted average interest rate of a mortgage is the sum of each rate multiplied by the amount in its loan. How do you calculate it? For each loan in the mixture, multiply its interest rate by the amount of money in that loan, then divide by the total loan amount.

If you look closely, you'll see that we do publish this figure — the weighted average interest rate — on the dashboard:

It's tempting to think this is a good metric, since the lower the average interest rate, the lower the total interest you pay and the cheaper the mortgage.

It's a very tempting metric to lean on, but it also opens the door to huge manipulations that can hurt you. You can lower mortgage rates through tough negotiation — but there are also "illegitimate" ways to do it. A bank can shift money from fixed-rate loans to variable-rate ones, or switch tracks that aren't CPI-linked to ones that are.

That will indeed bring the rates down, but it also significantly raises the risk in the mixture. The bigger the CPI-linked portions of the mortgage, the riskier it is.

The initial monthly payment you set when planning the mixture matters — but the payments over the following years matter just as much. Higher risk means a potentially larger jump in the monthly payment. The only time you can use this metric to compare mixtures is when the loan tracks, the amount allocations, and the loan terms are all identical.

❌Wrong method #2: Choosing the mixture with the lowest repayment ratio

The repayment ratio tells you how much you'll pay for every NIS you borrow. If, for example, the repayment ratio is 1.38, then for every NIS you take, you'll repay 38 agorot over the life of the mortgage.

Even though the goal is the cheapest mortgage possible, this metric can be a double-edged sword. You can only use it alongside the initial monthly payment. Because if a higher monthly payment is required, then in the big picture — once you account for your debts and cash flow — the mortgage may actually turn out more expensive.

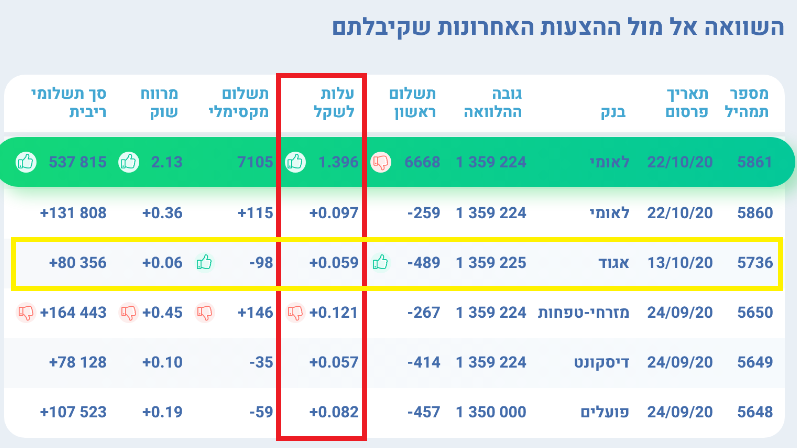

Let's illustrate with an example. We'll compare two offers: Bank Leumi's, with the lowest estimated repayment ratio of 1.396, versus the offer from Union Bank (Bank Igud), which is more expensive by 5.9 agorot per NIS borrowed.

But the parameter that fills in the rest of the picture is the first month's payment. Leumi's offer is indeed cheaper, yet it demands a monthly payment that's 489 NIS higher than Bank Igud's. Leumi's offer costs us about 500 NIS a month. Over 20 years, that's 117,000 NIS. How would that money grow if it were invested over the years? It may well be that a lower monthly payment actually frees you up for serious retirement savings, leaving you with more money overall.

Note: Bank Leumi's mortgage offer might finish earlier, sparing you unnecessary monthly payments that would narrow the gap again — so this deserves a close look.

So when can you compare based on the repayment ratio? Just like before — when the mixtures are identical in their loan tracks, the split of years, and the amounts in each track.

❌Wrong method #3: Choosing the mixture with the lowest monthly payment

Another wrong way to judge how attractive a mortgage mixture is: picking the one with the lowest monthly payment. This is a common manipulation in the later stages of negotiation. One of the banks can't compete with the rates the others are offering, so it stretches out the loans to lower the monthly payment — and bills itself as having the offer with the lowest payment.

When this happens, we actually take it as a good sign: it means the bank is about to drop out and the negotiation is winding down. That said, this move forces us to re-examine every mixture we receive and check that it still matches our original plan.

Fortunately, the mixture comparison table makes the trick easy to spot. We'll notice that one mixture has a lower monthly payment than the other but a higher repayment ratio.

The condition for using the first payment to compare mixtures is — you guessed it — that the mixtures share an identical structure: the same loan tracks, the same loan terms, and the same amount allocated to each track.

The right ways to compare mortgage mixtures

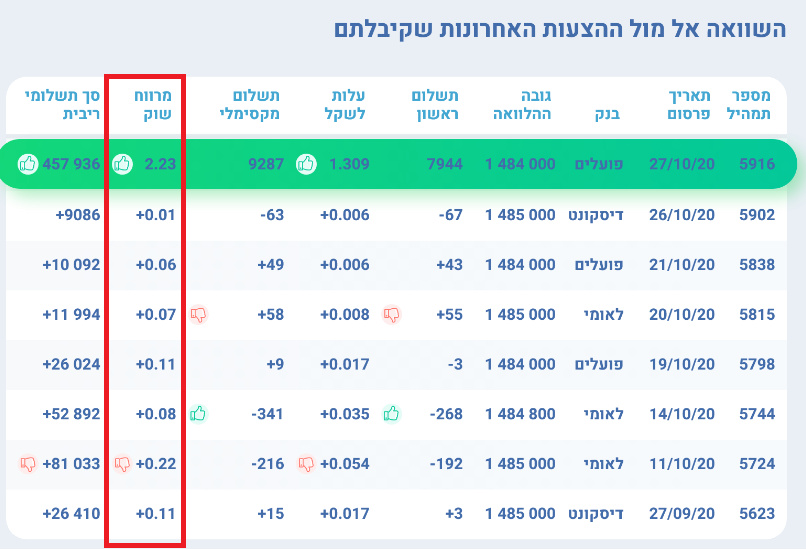

We've covered what not to do. Now let's talk about what to do. To compare mortgage offers, we'll use the market spread (with one exception, described below).

For anyone who doesn't want to read the whole article: the market spread is the weighted average of the gaps between the cost of raising the money in the capital market and the interest rate you got on each loan track.

The lower the market spread, the cheaper the rates you got. And here there are generally no tricks or gimmicks. If the bank switched you from a fixed unlinked track to a fixed CPI-linked one to lower the rate, the market spread will reflect that change. If the bank tries to lure you with one cheap loan while marking up the others, the market spread will tell you whether the offer is actually good. And by the way, that's not even the biggest advantage of using the market spread.

The huge advantage of using the market spread when comparing mortgage offers

The market spread lets you tell the difference in quality between offers even when they aren't exactly identical.

Say, for example, we're looking at a pair of offers from two different banks. Every parameter is completely identical (including the amount allocated to each track) except for the interest rate and loan term on the fixed unlinked (Kalatz) loans:

- In the first bank's offer: there is a fixed unlinked loan for 23 years at an interest rate of 3.05%.

- In the second bank's offer: there is a fixed unlinked loan for 24 years at an interest rate of 3.05%.

Even though the offers aren't identical (because the Kalatz loan terms differ), it's clear that the second offer is better than the first. The second offer has a lower market spread:

- In the second offer, shortening the Kalatz loan term to 23 years would yield a better interest rate (rates on fixed loans depend directly on the loan term) than the loan in the first offer. The second bank will reward us for shortening the loan and drop the rate.

- Conversely, if we extend the loan in the first offer by one year to 24 years, we can expect a higher rate than the one we got in the second offer. The first bank will penalize us for extending the fixed-rate loan and raise the rate.

When can you not use the market spread to compare mortgage offers

If you have a loan you plan to get rid of right away (say, to prepay it within a year), you can't use the market spread — because the number we show you includes the market spread of every loan in the mixture. In that case you fall back on the same rule: choose the loan with the lowest repayment ratio, but make sure the loan tracks, terms, and fund allocations are identical.

The bottom line: you might be a graduate of the IDF's elite negotiation unit, but if you don't know where you want to end up, or you have no way to tell a good mortgage mixture from a bad one, you're about to lose money. Mortgage bankers are good at their jobs and will spot it in a heartbeat if you aren't. The single most important thing — and we've said this dozens of times — is to know which mortgage mixture you're after. When you signal to the mortgage banker that you know exactly where you're headed, you'll get better interest rates.

Good luck!