How and When to Include CPI-Linked Loans in Your Mortgage Mixture

Loans linked to the Consumer Price Index (CPI), or to inflation, have the worst reputation of any mortgage track because of their potential risks. That said, when you combine them correctly in your mortgage mixture, they can make for a cheaper, shorter mortgage. In this article we'll cover what CPI-linked mortgage loans are, their advantages and disadvantages, and how to work them into your mortgage mixture the right way.

Background: What are CPI-linked loans?

CPI-linked loans are loans in which the principal (the outstanding debt) is updated every month in line with the Consumer Price Index. When the CPI rises, the principal rises too, and so does the monthly payment. Exactly how this works, including the compound interest effect, is explained in detail in the article on the effect of the prime rate and inflation on the monthly payment.

To get a handle on the basics of inflation and the Consumer Price Index, we recommend reading the article on inflation and the Consumer Price Index.

Types of CPI-linked loans

There are three main types of loans linked to the Consumer Price Index:

- Fixed CPI-linked loan (Katz) — fixed interest rate, principal linked to the CPI

- Variable CPI-linked loan (Matz) — variable interest rate, principal linked to the CPI

- Government-subsidized mortgage (Zakaot) — a subsidized loan with a fixed interest rate, principal linked to the CPI

Each of these loan types is explained in detail in its own article. Here we'll focus on when and how to combine them in your mortgage mixture.

What are the disadvantages of CPI-linked loans?

Let's start with the disadvantages rather than the advantages, because there's no ignoring them.

First disadvantage: The monthly payment climbs every month — slowly but surely!

The main drawback of CPI-linked loans is that the payment will rise every month, and most likely for the entire life of your mortgage. It's expected to rise continuously, because the Bank of Israel's monetary policy aims to maintain positive inflation at all times.

To drive home the risk in this expected growth of the monthly payment, we'll use the Rule of 72.

This is a financial rule of thumb for estimating how many years it will take the monthly payment (or, in its original use, the value of your investment) to double, given an annual inflation rate (or, in the original use, an annual return).

For example, if inflation is 3%, the Rule of 72 approximates the payment-doubling time as 24 years (72 divided by 3 equals 24).

Second disadvantage: We pay and pay every month (and have for a long time now), yet the debt to the bank only grows!

From what we described above about how the loan responds to changes in the Consumer Price Index, you can see that the loan principal can actually grow over time.

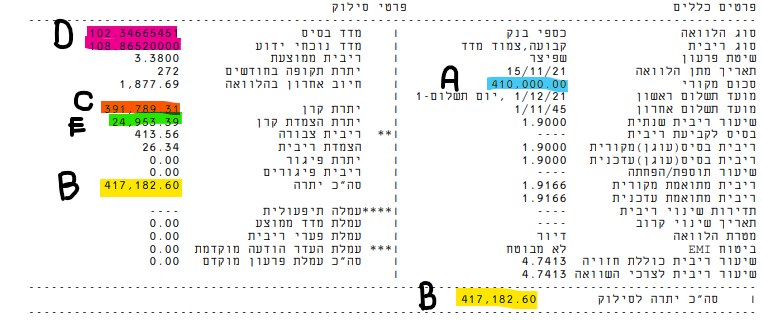

📊A real example — how the outstanding balance can grow in a CPI-linked loan

Below is a screenshot from a loan payoff statement issued by Israel Discount Bank.

A person took out 410,000 NIS (the blue marking, labeled A) in a fixed-rate CPI-linked loan on 15/11/2021, with an initial monthly repayment of 1,773 NIS. The loan carries an annual interest rate of 1.9%. The client was stunned to find, 16 months later, that even though his monthly payment had risen by 100 NIS/month over the original, his current outstanding balance was 417,182 NIS (the yellow marking, B) — that is, 7,182 NIS more than he actually borrowed.

How is this possible? Over this period, his principal actually dropped by 19,000 NIS to 391,000 NIS (the orange marking, C), but because the CPI rose (from 102.34 points to 108.86 points — the purple marking, D), the principal grew by 24,000 NIS (the green marking, E).

Let's reassure this borrower, and you too. This loan will end exactly on its scheduled date (1/11/45). The monthly payment rose precisely to overcome the CPI increase. But it bears emphasizing: when you take out a loan linked to the Consumer Price Index, the principal will very likely rise above the original amount.

What are the advantages of including CPI-linked loans?

After everything we wrote above about the downsides of this loan, you might think there's no reason to take one — but that's not the case. Used with full awareness of its risks, this loan has quite a few advantages. Let's run through them:

First advantage: Using a CPI-linked loan reduces the monthly payment

A mortgage, as we know, is a contract between you and the bank that lends you the money. Both sides want the same thing — for the whole debt to be repaid in full and on time. Within that shared interest, someone has to decide who bears the inflation risk. If you hand the inflation risk to the bank, so that the real value of the payments it collects each month is eroded by inflation, it will demand compensation in the form of higher interest rates on your loans. Conversely, if you bear the risk yourself, the bank rewards you with lower rates that bring the monthly payment down.

You can put the room this frees up in your monthly payment toward shortening loan terms and lowering the cost of other loans, giving you a cheaper mortgage overall. Since shortening loan terms is the single best way to cut the total cost of a mortgage (even better than lowering rates), a mortgage with exposure to CPI-linked loans will always be a cheaper one.

Second advantage: It reduces the early prepayment fee.

The early prepayment fee (also known as the interest-differential fee or discounting fee) is a fee the bank may charge if you want to repay the mortgage ahead of schedule. You might want to do that when refinancing the mortgage (changing its terms or composition) or when making a partial or full prepayment (reducing your debt to the bank).

The fee is set by regulation and rests on a very complex calculation, but one of the factors that directly affects it is your loan's interest rate. The lower that rate, the lower the early prepayment fee. So in certain situations it's worth considering CPI-linked tracks if there are amounts you plan to prepay.

Third advantage: Including CPI-linked loans in the mortgage mixture raises the profitability level of the mortgage portfolio and allows us to obtain better interest rates on the other tracks in the mixture.

Even though this is the most important point, the explanation is fairly complex, so feel free to skip it.

Let's start with a bit of background. The market spread is the way to capture, in a single number, the interest rate level of your entire mortgage mixture. It's calculated as a weighted average of the market spreads of all the loans in the mixture. We want the market spread to be as low as possible, so the bank profits as little as possible from our portfolio. Naturally, the bank wants exactly the opposite.

But what exactly is a spread? It's the difference between the interest rate you got on the loan and the rate defined as the " risk-free rate". The risk-free rate is a return you're guaranteed to receive on the loan you extend, and the one paying it is the State of Israel. The spread is the premium a financial institution demands to justify lending the money to you rather than to the State of Israel.

How do you calculate the spread of a single loan? By calculating the average (weighted) duration relative to the relevant yield curve. For loans that are not CPI-linked (fixed unlinked loans and variable unlinked loans), the market spread is calculated against the nominal yield curve. For loans linked to the Consumer Price Index, the market spread is calculated against the real yield curve. The Bank of Israel publishes the yield curves here.

The yield curve is a graph showing the yield of government bonds by the time remaining to maturity. The curve usually slopes upward — longer bonds offer a higher yield to compensate for the risk. It serves as the basis for mortgage pricing: banks take the government yield for the relevant term and add a spread that reflects the borrower's credit risk and the bank's profitability.

Nominal yield curve: Yields as stated in regular (Shahar) bonds, without taking inflation into account. This curve is the basis for pricing fixed unlinked loans and variable unlinked loans.

Real yield curve: The yields of CPI-linked bonds (Galil), reflecting a yield after deducting inflation. The gap between the two reflects the market's inflation expectations. This curve is the basis for pricing CPI-linked loans.

The real yield curve is lower than the nominal yield curve (generally by the inflation rate), and therefore CPI-linked loans carry a higher spread. They raise the weighted market spread, raise the portfolio's profitability, and therefore allow interest rates to be reduced on other loans.

Who are CPI-linked loans suitable for?

Now that we've covered the disadvantages and advantages of these loans, let's work out whether it makes sense to include them in your mortgage mixture. We'll lay out several reasons you might want a mixture with greater exposure to loans linked to the Consumer Price Index.

Our baseline assumption: for two mortgage mixtures with the same monthly payment, the one with CPI-linked loans is riskier (the payment grows every month) but also cheaper (you'll pay less interest in the end) than the one without them.

Before we begin — the conditions we think you should meet to include CPI-linked loans in your mortgage mixture

As we've shown, including CPI-linked loans in your mortgage mixture carries real risk. What happens if, shortly after you take out the mortgage, inflation rears its head and you start struggling with the monthly payment?

Consider including CPI-linked loans only if you meet one of the following conditions:

- Positive cash flow — to let you absorb an increase in the monthly payment

- Capital set aside — to let you pay off CPI-linked loans if inflation runs higher than you planned and allowed for

If you meet one of the conditions above, let's talk about when it makes sense to include CPI-linked loans in your mortgage mixture.

First reason to include CPI-linked loans: We're comfortable with risk

Just as the Consumer Price Index rises and pushes the monthly payment up, it can also fall — in which case the payment comes down. If inflation runs lower than expected over the years, we'll enjoy cheaper mortgage rates than we would on non-CPI-linked loans.

Of course, none of us can know what the future holds; we're "betting" on the inflation that will prevail over the life of the loan, so there's a degree of risk here that we need to be ready for.

Second reason to include CPI-linked loans: It's an investment property

The goal with an investment property is to earn a solid return on your investment. How do you measure that? The right metric is the return on investment (ROI). And the way to maximize it is to choose the cheapest mortgage — which is a mortgage linked to the Consumer Price Index.

When you rent out a property, it's common to renew and update the rent in line with shifts in market prices and inflation. If we can tie the rental agreement to inflation, we can hedge against the rise in the monthly payment that inflation causes, and so enjoy a cheaper mortgage.

Asset-Liability Matching is a financial principle that says you should match your income sources to your liabilities — so that when expenses rise, income rises proportionately to offset them.

In the context of an investment property: if you take out a CPI-linked mortgage, the monthly payment rises with inflation. To avoid a cash flow shortfall, you need to make sure the increase in rental income covers the increase in the mortgage payment.

Definitions:

- MonthlyRent - monthly rental income (NIS)

- MortgagePayment - monthly mortgage payment (NIS)

- MaxInflationRate - expected annual inflation rate (%)

- RentIncreaseRate - annual rent increase rate (%)

Formula:

Example: Monthly rent 5,000 NIS, mortgage payment 6,000 NIS, expected inflation 4%, rent increase rate 3%:

In other words, up to 62.5% of the mortgage payment can be CPI-linked without causing a cash flow shortfall.

Third reason to include CPI-linked loans: We are on the verge of a salary jump and/or a significant reduction in expenses

Say we're students, or about to be promoted, or there's some other reason our cash flow is set to improve significantly — but we still need to take out the mortgage now. The way to capitalize on that future cash flow growth is to choose a mortgage linked to the Consumer Price Index.

That way, we enjoy a lower monthly payment and get a cheaper, shorter mortgage (compared with a non-CPI-linked one). The payment will rise over the years, true, but our growing cash flow will leave us with enough headroom to handle it.

Fourth reason to include CPI-linked loans: Your income/salary is indexed to the Consumer Price Index

Salary indexation has grown less common over the years, but it still exists (mainly in the public sector). If your salary rises every year in line with the Consumer Price Index, then inflation-driven increases in your monthly payment won't hurt you, because your salary grows right along with them.

How should you take out CPI-linked loans?

There are two approaches to including CPI-linked loans in your mortgage mixture. The first aims to build the cheapest possible mixture (but carries more risk). The second aims to reduce the risk, but it's more expensive.

First approach to including CPI-linked loans: Cheap mortgage mixture, high risk

Since CPI-linked loans are the riskiest, they should be the shortest loans in the mixture (the ones with the shortest term). Why? The shorter a loan, the faster you pay its principal down. So if there's positive inflation next month, the principal grows from a smaller base.

This approach pushes the monthly payment up faster, because the shorter a loan, the bigger its monthly payment.

Second approach to including CPI-linked loans: Expensive mortgage mixture, lower risk

If we stretch out the terms of the CPI-linked loans, their monthly payment comes down. And if inflation rises 0.1% next month, the bump in the payment is gentler because the payment is lower to begin with. The downside is that a longer loan pays its principal down more slowly, so a rise in inflation triggers a larger increase in the monthly payment.

Want to see how different inflation scenarios would affect your monthly payment? Use our mortgage calculator and build a mortgage mixture with CPI-linked loans to see the effect for yourself.

Good luck!