Loan Fundamentals

Our task is to build our desired mortgage mixture. That is, we need to choose a number of different loans — usually between two and five (though it can be any number) — that will make up the mortgage mixture. For each loan we choose, we need to determine what type it is, how long it will be, how much money to allocate to it, and more. There are a few constraints, which we will mention later, on the composition of the mortgage mixture, but in general — almost anything is possible.

On one hand, this is excellent. We have a real ability to obtain a cheap loan that is perfectly tailored to our needs. On the other hand, this could lead to big losses — if we lack the knowledge required to construct the mortgage mixture. Every loan has advantages but also disadvantages.

Before we review each one individually, we want to establish a common vocabulary so we're all on the same page. We'll cover loan fundamentals — and in particular two core concepts: the bank margin and indexation. Indexation will explain how our future payment will change as a result of external influences. The bank margin explains how much the bank expects to earn on the loans it grants us.

The bank margin — one number that tells it all

The bank's role is to provide financial liquidity — to let us reach our financial goals even when we don't have all the resources we'd need to do so on our own. The bank is a business, and it wants and needs to make a profit. If it doesn't, it won't survive, and then there'd be no one to lend us the money to buy our home. The bank is going to profit from our mortgage. How much it profits, though, is entirely up to us.

As noted earlier, the money the bank lends us is itself borrowed from other sources. It can come, among other things, from customer deposits, from raising funds in the capital market (by issuing bonds), and even from trading in equities. Either way, the bank too has to pay for the money it borrows.

So how does the bank profit from our mortgage? It has to make sure the payments it collects on the loan it gives are higher than the payments it owes to whoever lent it the money. In other words, if the bank used John Doe's deposit to raise the money and grant us a mortgage, it needs the interest payments it receives from us to be higher than the interest it has to pass on to the deposit holder.

An example of calculating the bank margin

Let's walk through an example. Suppose the bank lends Efrat a sum of money at an annual interest rate of 5%. To fund that loan, the bank borrows the money from Yuval and promises to pay him an annual interest rate of 3%. So the bank earns 2% on this loan.

But hold on — that's not the margin yet. To sell Efrat the loan and borrow the money from Yuval, the bank had to spend on advertising, legal services, bankers to sell the loan, internet and computing infrastructure, and so on. All these costs, which we'll call operating costs, have to be deducted from the profit above (2%, remember?). If we assume they come to 0.8% of the total loan, then the bank margin on this loan is 1.2%.

This means that if Efrat borrowed 100,000 NIS, the bank earns 1,200 NIS on this loan.

Why does it matter to us what the bank margin is?

Nobody likes getting taken for a ride. So from the very moment we receive the mortgage offer, we'll want to know whether we got good interest rates (or not) on the loans that make up our mortgage mixture.

The margin is the single number that tells us, in terms of interest rates alone, how good our offer is.

The margin helps us focus. Say the bank tempts us to sign by offering a very cheap loan on a small amount, but charges very high interest on the other tracks. Because most of the money in the mixture is sitting in expensive loans, the bank margin will expose this and show how unattractive the mixture really is as a whole.

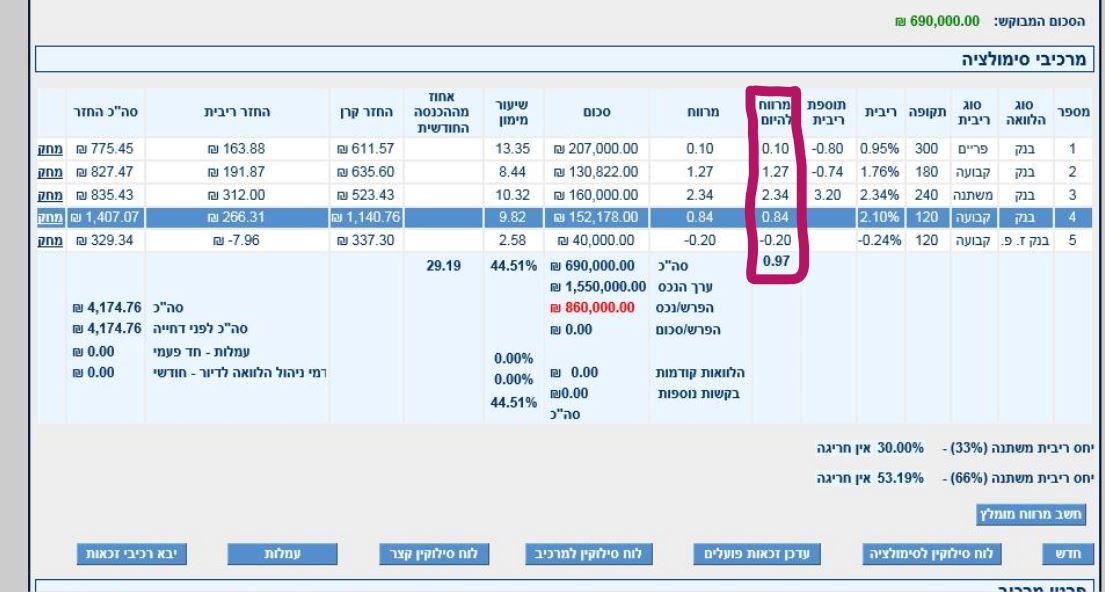

Take the image below, for example, from Bank Hapoalim's mortgage system. You can see the bank margin for each loan track. The higher the margin, the more profitable that loan is for the bank.

We can see that the prime-linked loan (loan number 1) is the least profitable for the bank, while the variable-rate loan is the most profitable. So if we want to drop the variable-rate loan from the mixture, we'll have to accept higher interest rates on the other tracks so the bank can still hit its profit targets.

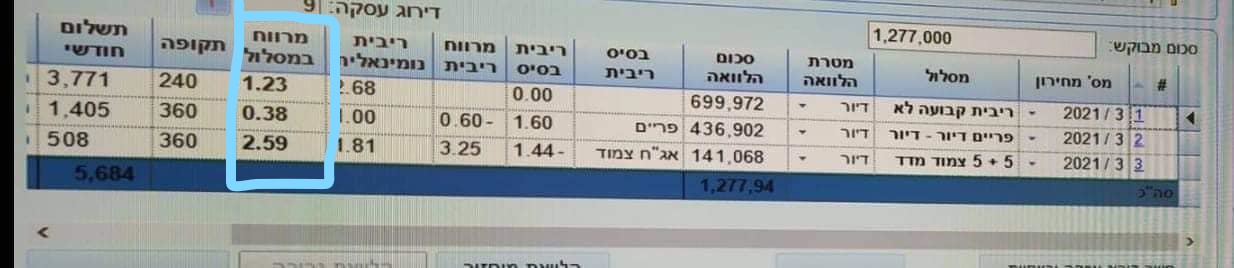

Here's another example, from Israel Discount Bank's mortgage simulator. Look at the spread column for each track. You'll see the prime-linked loan has the lowest margin, 0.38%, while the variable-rate loan is the most profitable for the bank, at 2.59%.

Loss leader is a term in marketing for a product sold at a loss to attract customers. In the case of the prime-linked loan, the bank may offer it at a low margin (or even a loss) to entice customers to take out the mortgage, hoping they will also choose more profitable loan tracks.

How do we calculate the bank margin or the market spread?

Unless we work at the bank, we have no way of calculating the bank margin. The screenshots above aren't available to us. We can't know the bank's operating costs — which themselves vary from bank to bank. And we don't know where it raised the funds for our particular loan — it could be from customers, the capital market, bonds, and so on. But don't be annoyed — we haven't wasted your time.

So what can we still do? A few things. First, on some loans the bank does specify the market spread. The market spread is the loan's spread relative to the cost of raising that loan in the capital market. The loan's anchor is the yield of the asset against which the money is raised — for example, the anchor of the prime rate is the Bank of Israel interest rate.

Bank margin is the bank's net profit after deducting operating costs.

Note: the market spread is not the bank margin!

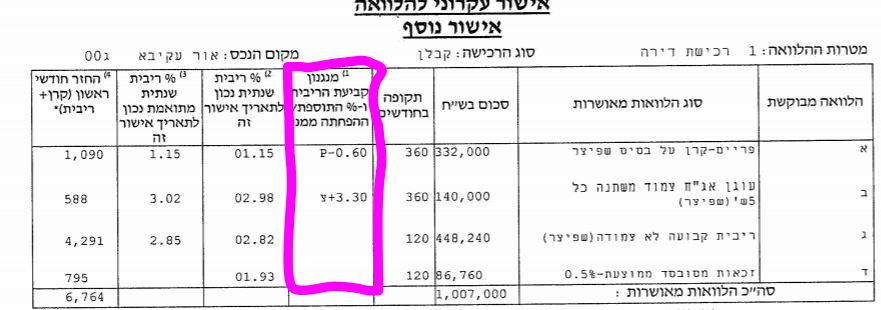

We'll expand on this in the units that follow. For now, take this mortgage offer from Bank Leumi. Ignore all the other information in it for the moment and focus on what's highlighted.

On the first loan, requested loan A, the market spread is minus 0.6% relative to the loan's anchor — the prime rate. And you can see that the second loan, requested loan B, linked to the government bond anchor, has a market spread of 3.3%.

For the two remaining loans, there's no breakdown of the spread. So the bank margin on these loans is worked out by calculating the average duration of the loan and comparing it to the interest rate currently on the Bank of Israel yield curve. We'll elaborate on this in the posts that follow.

To calculate the weighted average spread of a mortgage mixture, multiply the spread of each loan by the loan amount, add up the results, and divide by the total amount of all loans in the mixture.

Example: Suppose we have a mixture with three loans:

| Loan type | Term (years) | Amount (thousands NIS) | Spread (%) |

|---|---|---|---|

| Prime-linked | 30 | 300 | 0.8% |

| Fixed unlinked (KALATZ) | 30 | 500 | 0.5% |

| Variable CPI-linked every five years | 30 | 200 | 1.7% |

| Total | 1,000 | 0.83% | |

Calculating the weighted average spread:

The weighted average spread of the mixture is 0.83%

Indexation to the CPI / prime rate / government bond anchors

With the exception of one loan type — fixed unlinked to the CPI (known colloquially as KALATZ) — every other loan is indexed to an external economic variable or parameter. That means every time that parameter rises, the interest rate or the principal on that loan rises too.

Let's walk through an example. Suppose we borrow money from the bank on a prime-linked loan, and say, for the sake of the example, that the interest rate we got from the bank on it is 2%. This loan (and this one alone!) is indexed to the Bank of Israel interest rate. So when the Bank of Israel rate rises by 0.25%, the interest rate on our loan rises by 0.25% too, and its new rate becomes 2.25%.

This is a risk. At some unknown point down the road, the monthly payment can — and likely will — climb beyond what we planned and signed up for. So why were these indexed tracks pushed on us in the first place? Why complicate things?

Why do indexed loans exist at all?

The bank isn't out to get us. There's no obligation to take these indexed loans. You can take the entire mortgage amount as a fixed unlinked loan, and then you'd have a mortgage with no surprises and no changes. Sounds perfect, right?

Not quite. It's a very expensive, very long mortgage, and in our view it still means taking a risk — just a different one. But that's not really the point here. Just as we ask the bank for money, the bank borrows money from other sources to fund our loan. The bank too is exposed to all these parameters, so the name of the game is who pays the bill when the party ends and these variables rise.

When we borrow on the fixed unlinked track, we transfer all the risk (more precisely, the inflation risk) onto the bank. When inflation rises, the bank's profit erodes. So it demands a higher interest rate to protect its investment.

By contrast, if we take a fixed CPI-linked loan (KATZ), we share part of the risk with the bank. If those same variables rise, we pay more and the bank earns at least the same. And because the bank shares the risk with us, it gives us the money at lower interest rates.

So what do we do with the uncertainty?

Let's go back to the prime-linked loan. We can't know by how much or when the Bank of Israel interest rate will rise. And it's absurd to try to predict the future thirty years out. So there's an element of uncertainty here. If, over our mortgage term, rate increases run higher than we planned, it'll be an expensive, less worthwhile loan. If not, it'll be a cheap, well-suited one.

"It is difficult to make predictions — especially about the future"

Niels Bohr (1885–1962) was a Danish-Jewish physicist, Nobel Prize laureate in Physics (1922), who developed the Bohr model of the atom and was one of the founding fathers of quantum mechanics.

Since we can't know what will happen, we'll need to take an approach of saving while managing and hedging risk — something we'll cover at length.

Now that the concepts are clear, you can see them in action — try the mortgage calculator and build a sample mortgage mixture.

Good luck!