A Technical Explanation of the Mortgage — Nominal vs. Adjusted Interest Rate

The goal of this article is to introduce the basic terms of a mortgage — principal, interest, the nominal interest rate, and the adjusted rate. We'll see how the bank makes money and how we can pay down our debt to it.

The technical side — what principal and interest are, and the difference between the nominal and adjusted rate

First, we need to establish a common vocabulary. We'll use one example that we'll carry through the whole article.

We want to borrow one million NIS to buy our home. We've agreed that the bank will lend us the money on a twenty-year loan at an annual interest rate of 3.00%.

So the principal — the amount the bank gave you — stands at one million NIS. The bank, a business that lends money for profit, earns from interest payments. Interest is charged on the outstanding principal balance you owe it.

The principal is the sum of money borrowed.

Example: When you take out a mortgage of one million NIS, the principal at the start of the mortgage will stand at one million NIS.

Interest is the payment to the bank for the right to use the money.

Interest is calculated on the outstanding principal balance still left to pay. So as time passes and the outstanding balance shrinks, the interest payments shrink too.

The nominal interest rate is the annual interest rate stated in the loan agreement / principle approval.

The interest rate is annual, but it's calculated and paid monthly. Each month, a monthly interest rate is charged on the outstanding principal balance — in practice, the annual rate divided by 12. In our example, the monthly interest rate is 0.25% per month.

If we compound the interest each month at the monthly nominal rate without reducing the principal, we get the adjusted annual rate. This is the rate that shows up in the principle approvals you'll receive from the bank.

The adjusted rate is calculated by dividing the nominal annual interest rate by 12 and raising it to the power of 12 months.

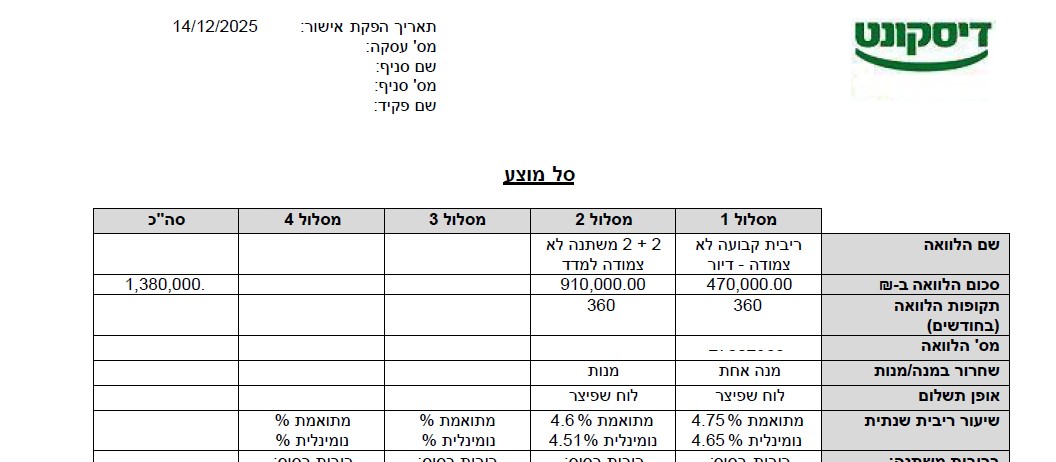

Let's use the following example from a principle approval issued by Israel Discount Bank.

- Track 1: fixed unlinked (KALATZ)

- The nominal interest rate is 4.65%.

- The monthly interest rate is 0.3875%.

- The adjusted rate is 4.75%.

- Track 2: variable unlinked (MALATZ)

- The nominal interest rate is 4.51%.

- The monthly interest rate is 0.3758%.

- The adjusted rate is 4.60%.

How the bank makes money

OK, back to our main example. The bank lent us one million NIS at a nominal annual interest rate of 3%. The monthly nominal rate is 0.25%, so after one month the debt to the bank will be:

How we reduce our debt to the bank

Building on the main example, let's say our monthly payment is 4,000 NIS. Out of that payment, 2,500 NIS — as noted — goes to cover the interest, and the rest, 1,500 NIS, goes toward reducing the principal (the debt) to the bank. So after that first payment of 4,000 NIS, the debt to the bank will stand at 998,500 NIS.

Looking at what happens next month, the debt grows by the monthly nominal interest rate, reaching:

Note! This month the bank earned only 2,496.2 NIS — approximately 4 NIS less than the previous month.

So our goal is to minimize interest payments and maximize principal repayment. The larger the principal portion relative to the monthly payment, the cheaper the loan.

Two important conclusions follow from this.

The first is that the principal starts shrinking from the very first month. The debt to the bank falls right from the first payment. If someone told you that at first the whole payment is interest and only later does it go toward principal — that's not true. If we paid only interest, the principal would never go down, next month we'd owe exactly the same interest, and the loan would never be paid off.

The second is that as time passes, the share of the monthly payment going to interest keeps shrinking while the share going to principal keeps growing. And as that happens, the bank's profit keeps declining.

Want to see everything you learned here in action? Go to the mortgage calculator and generate a full amortization schedule for all loan types.

Good luck!