What Is Cash Flow / How to Find Out Whether This Home Is Too Big for You

This article is about financial management and accounting for the most important business of all — your family. In particular, we'll dig into your family's cash flow. Understanding cash flow (a concept we'll explain here in depth) determines the cost of your mortgage more than any other factor. Yes, you can minimize interest payments by building a perfect mortgage mixture and haggling over interest rates like a market trader. But matching the monthly payment to your cash flow holds the greatest savings potential of all.

When income exceeds expenses, we have a cash-flow surplus. When expenses exceed income, we have a cash-flow deficit. Mastering our cash flow is the key to sound financial decisions: Can we buy a property right now? What monthly payment can we afford? And so on.

Say you need a one-million-NIS mortgage and you'd like to pay 5,000 NIS a month toward it. Before the mortgage, you were putting away 3,000 NIS a month and had no housing costs — so you had 3,000 NIS of spare cash each month.

The mortgage payment, though, is 5,000 NIS. Your 3,000 NIS of monthly savings covers only part of it, leaving you 2,000 NIS short every month (3,000 NIS saved − 5,000 NIS payment = −2,000 NIS). In other words, you're running a negative cash flow of 2,000 NIS a month.

The situation above clearly isn't sustainable. If your bank account is overdrawn, you're paying high interest on the debt and — worse — you risk losing your home. This is obviously something we want to avoid, which is why you have to figure out whether the cash-flow deficit is temporary or permanent (that's what we'll do now). If the deficit is permanent — meaning you don't foresee any change that will balance your cash flow — then you've picked a house beyond your means, so walk away from the deal. If you lose the home, your chances of getting financing and another mortgage down the road plummet.

A temporary cash-flow deficit, on the other hand, is a different story. Right now you have real, concrete difficulties keeping your income and expenses balanced. Such a difficulty can stem from any number of things:

- Double housing costs: you have to pay rent and a mortgage at the same time.

- A tricky employment situation: switching jobs, starting a new business.

- Other financial commitments: private daycare, university fees, loan repayments, and so on.

Later on, we'll discuss the tools available for dealing with this obstacle, but first we have to understand what our monthly cash flow is now and in the future. We have to figure out whether the cash-flow deficit will be temporary or permanent.

How to understand your cash flow

The next task is a challenge. You need to project what the movements in your bank account will be over the coming years. If you can do that, choosing the right financing program becomes easy. You're going to be the accountant for the most important business there is — your household.

To do this, you need to estimate four different numbers:

- What is your average monthly net income today? Let's call this variable current income.

- What is your average monthly expenditure today? Let's call this variable current expenditure.

- What future changes do you expect in your expenses? Let's call this variable future expenditure.

- What future changes do you expect in your income? Let's call this variable future income.

Your current cash flow is current income minus current expenditure.

Your current cash flow tells you whether you need to include grace-period loans in your mortgage, whether you're ready to take out the mortgage now or should put it off, or whether you can afford to buy a home at all right now.

Your future cash flow is future income minus future expenditure. It tells you how large a monthly payment you can afford and whether you'll be able to make early prepayments on the mortgage.

Future cash flow = Future income − Future expenditure

Estimating your current income

How much do you bring in, net, every month? Of the four questions above, this one is the easiest to answer.

First let's deal with earned income. This part is straightforward. If you are:

- Salaried employees / business owners: Review and average the deposits your employer has made to the bank in recent months. The bank will recognize this income if you can show pay slips and regular deposits in the account.

- Self-employed: Work with your accountant to pin down your after-tax profits. The bank will recognize this income once you provide tax assessment reports from previous years and a confirmation from your accountant of this year's income.

Moving on. Let's look at monthly income that isn't earned income. Add the following, after tax: scholarship income, pension payments, annuity income (only if you can prove it's permanent), alimony payments (not always recognized), rental income (after tax), monthly payments from assets abroad, and so on.

- The income comes in every single month, into your bank account.

- You have supporting documentation showing your legal right to receive the income (confirmation from the National Insurance Institute (NII), property ownership in the Land Registry (Tabu), a rental agreement in your name, scholarship eligibility confirmation, etc.).

- There is a match between the income statements and the deposits in your bank account.

- You have paid taxes on the income as required by law.

Finally, we'll add non-monthly income. Sum up all liquid income (that is, income that lands in your bank account) from dividend payments (only if you're a major shareholder in a company), quarterly payments from distributing funds, and the like. Divide this sum by 12 — and that's the monthly addition to your income.

One thing to stress: the bank won't recognize the income above as income, but it still matters for calculating your cash flow.

Estimating your current expenditure

Compared with the previous task, this one is harder. We need to figure out how much we spend each month running our household. That's tricky, because our needs shift constantly with our whims and circumstances. On top of that, our monthly expenses are volatile: in August we go on holiday, in June there's the car's annual service and inspection, and for the first ten months of the year we pay university tuition.

How do we handle this? We'll use historical data to calculate the average monthly expenditure. And how do we do that? With those wonderful Excel skills of yours.

📊Click here to learn how to calculate your cash flow using Excel(Excel guide)

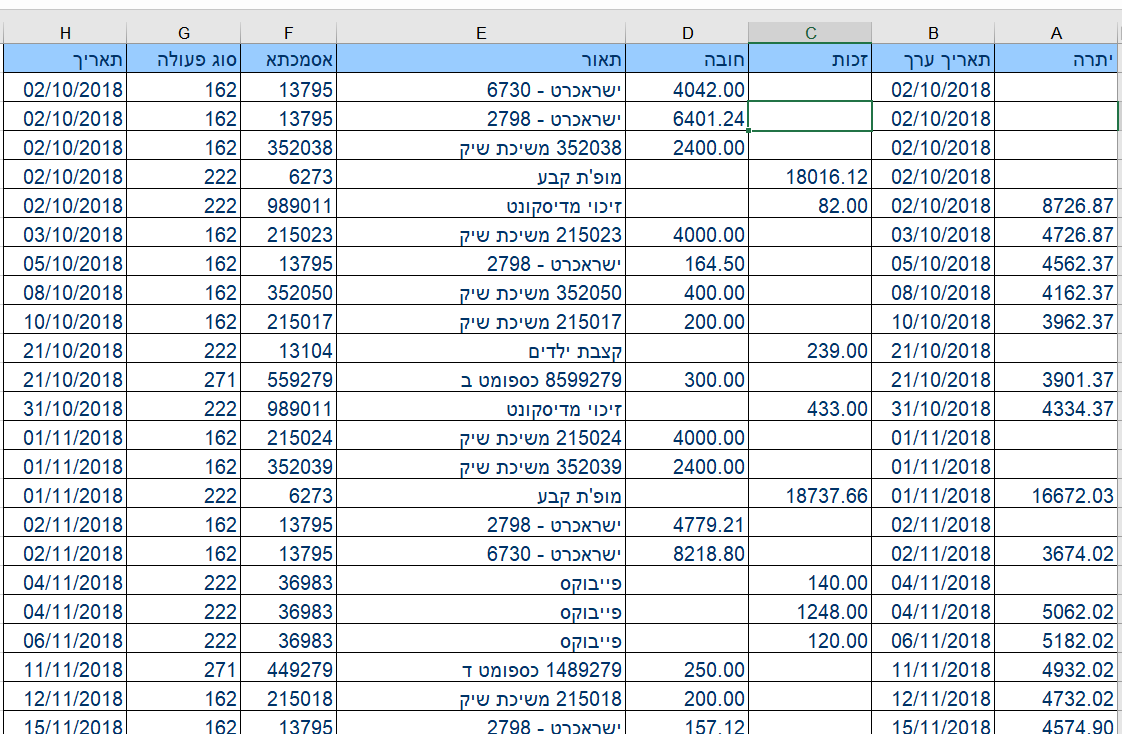

Let's begin. Log in to your bank's website and export your current-account transactions from the last eleven months to an Excel file. We'll say it again — the last eleven months.

On the one hand, you want as long a period as possible, because the more observations you have (the more months to work from), the more accurate your estimate will be. On the other hand, if you include December twice (this year's and last year's), your December expenses will be inflated and skew the figure you get.

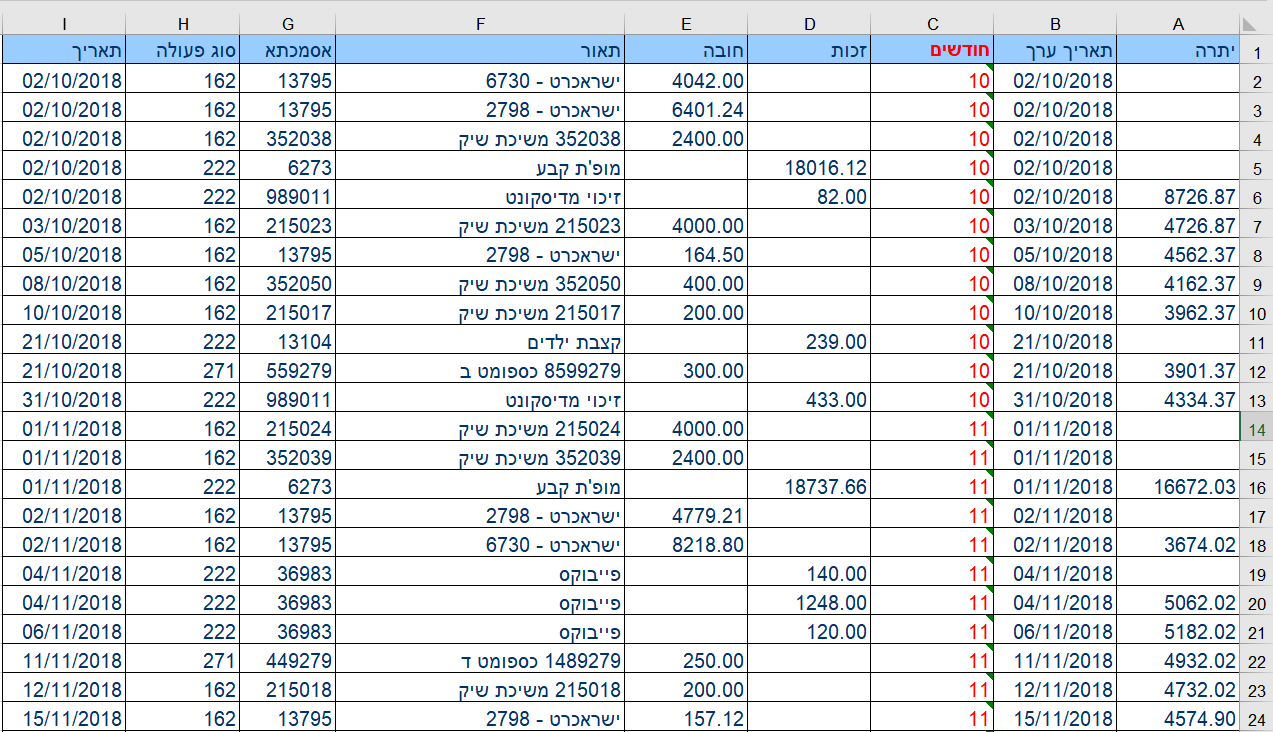

The columns we care about are the date column (column B) and the debit column (column D). Add a new column — this will be the months column. Be sure to give the column a name. Click on a new cell inside the column you just added — say, cell C2.

Enter the following formula in that cell: =TEXT(B2,"mm")

Run the formula down all the rows. Excel will pull the month out of the date for every value in the column. It'll look like this:

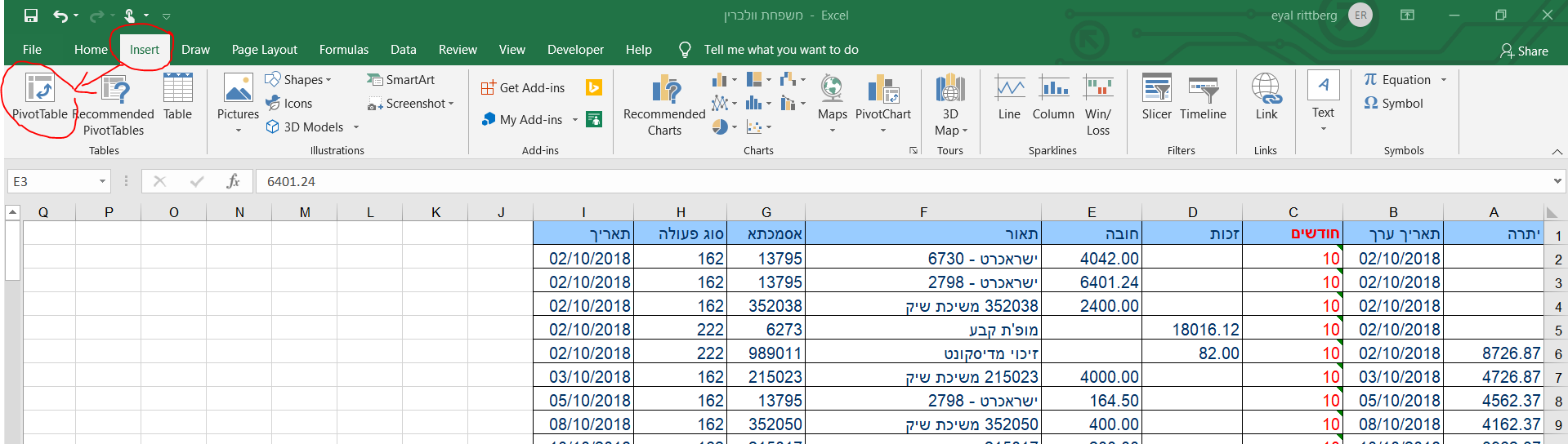

OK. Now we're going to use a Pivot Table. If you didn't know what a Pivot Table is until now, we're about to change your world. For anyone who uses Excel often, this is worth at least an extra 2,000 NIS in salary.

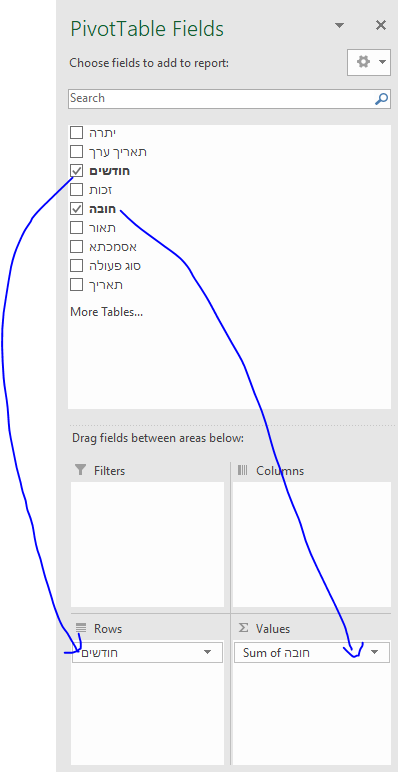

Select Insert → Pivot Table:

A new sheet will open where you define the Pivot Table. Drag the "Month" field into the Rows area and the Debit field into the Values area. Make sure "Sum" is selected in the Values area (the default is usually Count).

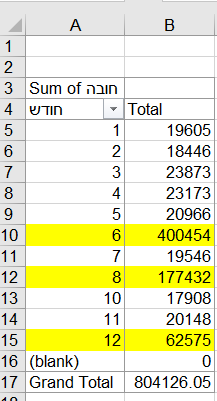

You have finished creating your table. Look at what you created:

You've effectively built a table that lays out exactly what your expenses were in each month over the past year.

Now take a look at what happened in June, August, and December — the expenses were unusually high. If we average across all the months, we get an unreasonable average monthly expenditure of 73,102. That's because we have three observations (those three months) whose expense structure is very different from the rest. In data science terms, these are called outliers.

To get a more accurate answer, we have two options. The first is to use the median, since it isn't thrown off by outliers. I won't go into that method here, but will focus on the second: go back to the data, figure out what's driving these high charges, and simply remove them from the file. If we sort the expenses from highest to lowest:

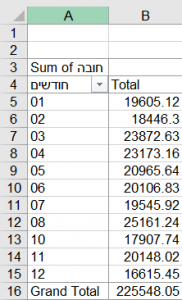

We'll find that the high charges in June and August come from paying payment vouchers for a home purchase, and that December had three one-off bank transfers leaving the account. If these really are one-off expenses, delete them.

After deleting these rows, we get the following expenses:

Now our average monthly expenditure stands at 20,504 NIS a month. Congratulations — we've figured out how much we spend. That's a huge step. Remember this number; it matters going forward.

Required adjustments to the expenditure calculation

The calculation you just did holds only if nothing changed in your expense structure over the 11 months you reviewed. If, for example, you enrolled your child in private education mid-year, or your fuel costs jumped mid-year, you'll need to make adjustments.

First adjustment: a permanent change in expenses. What do you do if for part of the year you had one expense structure and for the rest a different one?

A concrete example: for the first three months of the analysis, your child was at home with you during maternity/parental leave, and afterward entered private education at 3,000 NIS a month.

Two ways to handle this:

- Take only the most recent months with the updated expense structure. The catch is fewer observations and a less accurate estimate. In our example, that means using only the last eight months.

- Or artificially add the expense to the months before the change kicked in. In our example, you'd add 3,000 NIS to the expenses of the first three months, fully reflecting the change.

Second adjustment: a large recurring expense that didn't fall within the analysis period.

A concrete example: you replace your car every three years (36 months — this is the cycle time), spending roughly 36,000 NIS each time. It didn't happen during the analysis period, but it's coming up soon.

The fix: divide the expense by the cycle time and add it to the average monthly expenditure you found. In this example, we divide 36,000 NIS by 36 months to get an extra monthly expense of 1,000 NIS — which we add to the average monthly expenditure we calculated earlier (20,504 NIS).

Future changes - increases in income and increases in expenses

OK, so far we've learned from our past behavior. Now it's time to look forward. A sound mortgage is one that fits your family's needs and financial challenges. Those needs are dynamic and ever-changing, but if you put some thought now into shaping the mortgage around them, you'll be able to meet them far more easily.

The next task is to look into the future — to imagine what your life will look like over the medium term, within sight.

When does that future arrive? Necessarily after you've moved into the home you bought (say, once construction is done) — it has to be after the whole mortgage saga is behind you and you're already on your balcony counting migrating birds. Two years is usually a good timeframe. If you're a couple without children, we typically look four years ahead — by which point you'll have two kids (congratulations!).

Estimating future expenditure

You've reached that future. Let's look at the changes in your expenses. So far you've been spending on average about 20,504 NIS a month. Now you need to work out how your expenses will change. Look at your current expense structure and estimate the changes you expect for those expenses going forward. Things to consider:

- Transport: Until now you lived in location A; going forward you'll live in location B. How will your transport costs change? Will you buy another car? Will you have to fuel up more often?

- Home expenses: electricity, gas, water, municipal tax — how will these change? Do you have a garden to maintain? Are you moving to a building with more elevators where the building management fee will be higher?

- Insurance: Do you currently have life and property insurance? Do you have personal life insurance? Do you intend to assign your private life insurance to the mortgage? If you don't have children, you may not carry much insurance — but once you become parents, in my opinion, you need to load up on insurance and protection. Use our life insurance calculator to price this expense.

- Food: How will your food costs change going forward? Do you currently rely on your parents to cook for you?

- Children's expenses: How will spending on children change? Will you grow your family? When will the kids move from private to public school? Will you need extra help in your new home? We usually price the basic cost of raising a first child at 5,000 NIS and a second child at 3,000 NIS (though prices obviously vary by location and other factors).

- Housing: When you move into your shiny new home, you'll stop paying rent but start paying a mortgage. How will your housing costs change? If you've been paying 4,000 NIS in rent and now pay 5,000 NIS on the mortgage, that's a 1,000 NIS increase in housing expenses. If you're considering a relocation, the change will be even more involved — read about financial planning ahead of a move abroad.

- Lifestyle budget: How will your restaurant budget change? Trips abroad? Gadgets you'll buy? You may have lived like ascetics for the past two years to fund the home, but going forward, you'll want to let loose and live the life you want.

- Savings allocation: How much are you currently setting aside, on your own, for yourselves and your children? How much do you plan to save for them in the future? Saving isn't an expense, but you are pulling money out of your current account now to make it happen. Note: illiquid savings such as study funds (keren hishtalmut) without the required tenure, pension insurance, and managers' insurance (executive insurance) don't count as savings — only funds you've actively pulled out of your current account do.

- Loans that are ending: Are you paying off a car loan or a renovation loan? When do these loans end? What monthly payment will free up for you?

- Allocation for early prepayment: If you plan to prepay 60,000 NIS of the mortgage in five years, that's money you need to start saving today. In other words, you have to set aside money every month toward that prepayment.

Did we forget anything? If there's another item that fits your lifestyle, add it, of course.

Sum up all these expected changes and add them to your current expenditure — that's your future expenditure.

Estimating future income

This task is usually easier. If you're salaried employees, you should know the shifts in your salary structure. If you're not sure how much you can earn, there are plenty of salary tables to help.

Make a gender adjustment. Men and women have different expectations regarding the development of their salary. If you're a man, you're probably brimming with confidence and sure that in four years you'll be earning at the top of the salary scale — and climbing even higher. Women do exactly the opposite: they're pessimistic and aim lower.

Do yourself a favor — aim for the average of the future salary table. Remember that the growth figure is gross, not net; if you like, use gross/net calculators to work out the change in net salary. If you don't know how, use this (very rough and imprecise) rule of thumb: multiply the salary growth by half if your income is above 25,000 NIS, and by 0.66 if it's below.

If the property you're buying is an investment property — meaning it'll be rented out — you need to factor in three main variables:

- Wear, repair, and tenant-turnover costs in the rental property — what are the repair costs? Is there a chance the apartment will sit vacant? It's customary to multiply rental income by 0.95 to reflect these risks.

- Income tax on rental income. How will you be taxed? At 10% from the first NIS? On the exempt track? Subtract the tax from the rental income.

- Offsetting mortgage payments against rental income — how much of the rent is left after you pay the mortgage on the property?

Add the changes in income to your current income, and you have your future income.

Summary and final review

That was long, but you've reached the goal. Calculate your current cash flow and your future cash flow the way we described above. Once those numbers are in hand, setting the monthly payment is easy. You just need to choose a payment that doesn't tip you into negative current or future cash flow.

If you can't land on a monthly payment that allows this, then you have a problem. Put gently — you need to reconsider buying the home. Consider postponing the purchase until your finances improve.

- We recommend keeping your future cash flow at at least 10% — that is, keeping expenses to no more than 90% of your income.

- Raise that percentage if you're self-employed, a business owner, working an unstable job, or dealing with other unstable factors in your life.

- Lower it if you have a strong financial safety net and significant equity (unrelated to the mortgage).

If your future cash flow is balanced — meaning very close to zero — you've planned with razor-thin safety margins, and your ability to handle the unexpected (a layoff, a child with special needs, labor-market shifts, a car written off as a total loss, a burst pipe, a medical issue, orthodontic treatment) is limited. We recommend going back to the drawing board and seeing what you can change. Cut savings? Cut expenses? Rethink your family planning?

The next step is to find the right way to bridge the gap between your current cash flow and your future cash flow — that is, how to safely get through the period where you have to pay both a mortgage and rent at once, because the apartment isn't ready yet.

Good luck!